Will the Tax Working Group actually address housing inequality?

Grant Robertson instructed The Tax Working Group (TWG):

“to consider a package or packages of measures which reduces inequality, so that New Zealand better reflects the OECD average whilst increasing both fairness across the tax system and housing affordability“.

Inequality is a number one issue for Western countries like the US, UK Australia and New Zealand. It not the same as the poverty issue. The growth in extreme income and wealth differences has gathered momentum as tax-free gains accumulated at the top end compound asset values, while disadvantage and debt compound negatively at the bottom end. The fortunes of the top and the bottom are inextricably linked. To begin to reverse the growing wealth divide, policy must address the balance sheets of both.

But the TWG have both hands tied behind their collective backs by the terms of reference that excluded:

- Increasing any income tax rate or the rate of GST

- Inheritance tax

- Any other changes that would apply to the taxation of the family home or the land under it, and

- The adequacy of the personal tax system and its interaction with the transfer system

The TWG interim report and the two conferences last week suggest that at best the TWG will offer a realised capital gains tax that will be enormously complicated and politically fraught. In terms of fairness, that may improve some aspects of horizontal equity, sometime in the future, but only if capital gains, not capital losses, are made.

The controversial and complicated issues around the introduction of a comprehensive capital gains tax on realisation by 2021 include: the timing of the valuation of all assets, how they are valued; lock in and roll over problems; valuing goodwill; defining the excluded family home; allowing for inflation; holding assets for different time periods; and what happens on death.

Can anyone see the Labour government embracing a comprehensive capital gains tax to take into the 2020 election? National are not co-operating on this one and have promised to reverse any legislation. The last time Labour produced such a blueprint (the 1989 consultative document on the taxation of income from capital) they abandoned all of it as they entered the 1990 election.

In light of these challenges it appears that some TWG members would prefer an incremental to a big bang approach: building on the current capital gains policies such as bright line tests and ring-fencing rental losses and including more asset classes gradually.

What might they have come up with if they focused on the real housing inequality problem? To start they would refuse to be bound by the terms of reference that make their task impossible.

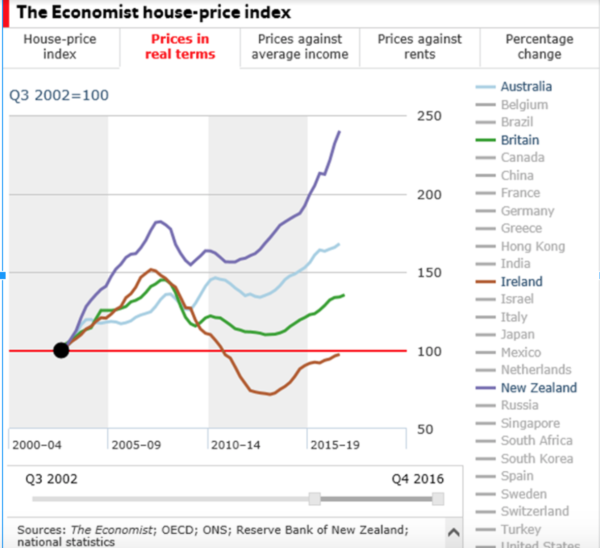

The kind of inequality that has been the most damaging is not trading in shares or Art collections. It is surprise, surprise, housing. Runaway fortunes have been made in real estate and New Zealand is chart topper in unaffordability of housing as the Economist shows.

Ireland used to be in the place that New Zealand now occupies. There may be a decade of capital gains tax losses in store for NZ such as happened in Ireland when the inevitable crash came. The exemption of owner-occupied housing for the TWG capital gains tax is another nail in the coffin. As in Australia this will just encourage an even worse over-investment in the exempt family home.

The sad fact is that a 7 % annual capital gain sees the $10milion mansion become a $20m mansion in just 10 years. This week the NZ Herald reports a couple who bought their Herne Bay home for $27.5 m after selling their Remuera property for $25.5m to a Chinese buyer. That same couple are reported to have bought an Auckland property for $3.9 million and sold it four years later for $62.8m.

One would hope that the later sale falls within the ambit of the existing bright line test. But even with a comprehensive capital gains tax, the likely considerable gains on the family home are exempt.

Scarce resources of labour and materials are sucked into the expansion of the luxury mansions built for the wealthy along with the resources for their maintenance, gardening and smooth operation. Often foreign-owned and lavish in the extreme, they are far more than a family home. This tragic misallocation of resources has been at the expense of basic housing for low income people.

Like food and education adequate shelter is a fundamental human right. But instead it has become a commodity to be hoarded and then traded for profit. Houses bought by investors too often are not even rented. Those that are rented, frequently offer no security of tenure, generating tax deductible losses for the owners while they wait for capital gain. In such a world any talk of economic efficiency in tax design rings hollow. How can inadequately housed families facing uncertain futures and multiple shifts produce children who are ready and able to learn? How can housing transience support their parents to be productive workers.

A different TWG might have sought to reduce the wealth divide rather than focus on tax on possible future capital gains. The Risk Free Rate Method (RFRM) or net equity approach would be considered a serious policy option to achieve a meaningful reduction in housing inequality by generating certain revenue and changing the attractiveness of investment in housing.

Under a net equity approach all housing wealth would be aggregated and only registered first mortgages deducted to give a person’s net equity. It would aim to affect only the top 20% of wealthiest property owners and absentee owners by allowing an exemption of maybe $1million against the person’s family home ($2 million for a couple).

The logic is that had the person had this net equity in cash it could earn a return on fixed deposit, so the housing net equity is treated as if on term deposit earning 3-4% taxable interest. Current 5 year bright line tests would be retained for short term gains.

Most of the problems of the comprehensive capital gains tax disappear- roll over, lock in, timing, inflation, accounting for capital expenditure. All houses and land zoned residential would have an official CV at the beginning of the year. Any mortgages repaid during the year would increase net equity. Of course, young people with high mortgage debt would have little net equity while older people who benefited from past gains would have more. The exemption of $1 m net equity for the family home means that the vast majority of people would be unaffected.

Landlords would no longer be able to write off interest costs or generate rental losses. They would not have to pay accountants to determine what is capital and what is deductible expenditure. All they would do is pay the tax on the interest imputed from their net equity. Accruing capital gains would be captured as they inflate the net equity base. If there is a serious crash then net equity would fall as the CVs fall.

Landlords would have an incentive to rent their houses and not just let them stand idle. Overseas owners would not have any family home exemption and any home held by a trust would not have an exemption either. Home owners would be free to generate income from Airbnb, boarders flat mates and home offices to help meet any net equity tax.

Most importantly the net equity tax would divert resources from luxury housing and change the culture of housing as an investment commodity leading to a much better use of housing stock. Revenue generated could be diverted to repairing the balance sheets of the worst-off by repaying debt and enhancing their asset accumulation.

Regarding housing inequality, I agree there is a housing crisis and increasing homelessness. However, there is NOT necessarily a shortage of homes/rooms .. hear me out ..

The advertisers that fund the main-stream-media desperately want property to continue to rise and failing that, plateau! The panegyrics towards rising property values has been nothing short or sickening propaganda.

The truth is many media outlets here are so scared of an alternate narrative, they’ve banned links from the likes of Martin North’s (DFA – Walk The World) YouTube channel.

There are many empty houses, and properties ‘coming on stream’ in NZ. The problem has been the housing bubble BUT it’s about to deflate! I could be wrong, but you’d be a fool to think otherwise given the evidence .. once you’ve taken the horse blinders off and looked around.

It would be expected to deflate on past form but we might be in a new era of financial intervention since the QE response to the GFC. Creating unlimited amounts of Fiat money to arrest a market/banking collapse wasn’t done in the past. Now I believe the authorities in the major economies are quietly supporting stock markets around the world whenever they look shaky with fiat money without any announcement..

That will flow through to housing markets as more and more money is thus fed into circulation, looking for safe if not profitable investment. This is enough to keep the bubble expanding as long as it goes on. The stock markets are already dislocated from sensible dividend relationships but there’s nowhere but shares and property for the money to go.

It is just going to separate those that have access to this inflationary money from the masses that do not.

Traditionally inflation has pervaded the economy of the people, in food prices , consumer goods etc. But in this situation little of the inflationary money is entering the real economy, because there is no attractive investment in the real economy of ordinary people. The gap is set to widen at an ever increasing rate between the haves and the have nots.

D J S

So has it been a waste of time?

I am sure you know the answer.

“But the TWG have both hands tied behind their collective backs by the terms of reference that excluded:

* Increasing any income tax rate or the rate of GST

* Inheritance tax

* Any other changes that would apply to the taxation of the family home or the land under it, and

* The adequacy of the personal tax system and its interaction with the transfer system”

And by the government having excluded all this, they have already ensured that the system will only get a few tweaks and trimmings around the edges. Expect damned little to solve anything, I reckon.

You can try and design a better performing and fairer tax system, including a capital gains tax of a form, or alternatively tax land, property higher, which is though already happening in the form of rates levied by local or regional authorities.

What I note though is, that the countries with the highest residential real estate price increases, the fastest growing valuations, they tend to be countries with relatively high net immigration rates. Look at New Zealand, Australia, Canada, and until not so long ago also the UK, and a few years back Ireland.

If you add, that is in the case of New Zealand, the many returning residents and citizens, who may have earned well overseas, then the immigration growth in this country is significant.

Add also some forms of overseas residential property investments, which was easier in years past, lesser so now, but still possible, we have a residential real estate market with high demand, not met by building of additional stock.

Anecdotal evidence indicates that potential foreign buyers are still very much present at open homes and auctions.

As long as we have this comparatively laissez faire immigration allowed into New Zealand, as long as some back doors seem to exist, and as long as governments of both sides of the political divide consider growth, also achieved through growing the population, as being the ultimate goal, we will continue to have rising land, house, unit and apartment prices across New Zealand.

Restrict immigration and contain population growth, and prices should ease, while the work force gets trained to build more homes for locals only.

We need more productivity, we need to focus on what matters and represents the essentials for living decent lives, and it can be done. But instead, we have a middle and upper class obsessed with getting the latest imported cars, improvements to their homes, new boats or motorbikes, the latest gadgets and overseas holidays, also spending much on consumerist trash goods, wasting money that is needed for more essential spending.

Inequality is an issue, poverty is an issue, but those that have do not want to share, they prefer their quarter acre sections, gated communities and leafy suburbs, other ‘riffraff’ kept well away in the ghettos destined for them.

An obsession with the need for a capital gains tax on housing speculation can only be maintained by someone not understanding how little speculation in housing can be done without the speculator being deemed by IRD to be a dealer, and paying income tax on the speculative profit at a far higher rate than anyone is suggesting for a capital gains tax. Or how easy it would be to make the criteria for being deemed a property dealer even more encompassing.

The problem is international and systemic. The gains achievable in the present environment with property prices driven both by our immigration requirements re financial qualifications, and the unlimited amount of money in the world looking for a return on investment mean that almost any tax for those with cash to play with is almost irrelevant. It’s what’s left over that counts. And alongside investing in government bonds at zero or negative returns , speculating in the Auckland housing market even at over 50% capital gains or income tax will always be the obvious choice while the bubble continues to grow.

Such a tax will catch all the wrong people.

If I have understood the suggested above (and I have tried), a net equity tax on a deemed value CV at 3 or 4% would be imposed. I suggest that this would be of little concern to a speculator with cash burning holes in their pockets, but a serious concern to a young family stretching their resources to secure a home. At the present rate of house price inflation $1 or $2 M exemption will not be a help for long.

The government has moved in the right direction limiting overseas money investment. This area together with including overseas money coming in with an immigrant , who buys their right to emigrate with that very same money needs attention.

D J S

David

you say “If I have understood the suggested above (and I have tried), a net equity tax on a deemed value CV at 3 or 4% would be imposed. I suggest that this would be of little concern to a speculator with cash burning holes in their pockets, but a serious concern to a young family stretching their resources to secure a home. At the present rate of house price inflation $1 or $2 M exemption will not be a help for long.”

Under the net equity approach as outlined a young family would be very unlikely to be caught up. The exemption is for net equity, not the price of the house. If the couple has a $3 million house and a $500,000 mortgage- each would have a net equity after the exemption of $250,000. If it was in the bank at 4% this is a taxable income of $10,000. If she is not earning that would be tax to pay of $1050 and $3,300 by the main earner on 33% tax rate. This is not onerous.

The couple in the example with a 27m home would each have $13m net equity. the net equity tax is highly progressive and wont affect 80% of people

I still can’t get it Susan. If a couple have a house worth $3M and a mortgage of $500 000 , then they have between them an equity of $2.5 M surely, not $250 000. What am I missing?

D J S

So if your income as an employee is $50,000 and your total capital gains is $20,000 then you total taxable income is $70,000.

HI David

each have an net equity of 1.25m in their family home. Each have a $1m exemption on the family home

Therefore each has a net equity of $0.25m. That if placed on the bank earns the interest they are taxed on.

Had the home been owned instead by foreign owners or as a second home net equity would be the full amount without an exemption .

Susan,

Will the Tax Working Group actually address housing inequality?

No; – they wont. nor will they repair all the damages NZ suffered since 2008 with all the asset stripping and privatisation.

With ‘MC Scrooge’ in charge of our public purse we cannot expect a ‘awakening of our past egalitarian society’ any time soon sadly as he should have used the “reserve bank act” to make Government’s own funding available for our massive funding for repairing the damages of the previous nine years of rort and slash and sale of our assets during the John Key years.

They should have followed what NZ Labour did during the first global depression under Michael Joseph Save in 1935 he used the Reserve Bank Act to fund social changes and enrich New Zealanders wealth and health and so should we now.

https://nzhistory.govt.nz/media/photo/michael-joseph-savage-1935

“The key election issue was the Social Security Bill, the embodiment of Savage’s welfare vision for New Zealand. This comprehensive policy of looking after New Zealanders from the ‘cradle to the grave’ helped ensure a comfortable Labour victory.”

Their CGT cannot address the accumulation of housing assets at the top end because that is gains made in the past.

They also cant include the family home- so $20m mansions are exempt

Well at least Roberston isn’t accusing Qatar of terrorism so the other OPEC nations can kick Qatar out.

It is worth noting how ever, Susan also asked made the point about the governments intentions particularly since we’ve seen a decline in the revenue of the construction industry. The former government lived in the junk food days of Mainzeal and all that easy lazy money coming out of those big real estate investment trusts and all those big pools of money coming out of public private partnerships are now finished or are in the gym been nets secondary recovery.

But I don’t believe that a consumption tax cut in GST can cut marginal tax rates. Tax can’t go up on the big end of town. Neither can it go down at the bottom end. Where it was possible in the past it’s not possible now. Another reason is because we have restricted goods going untaxed like the family home. The base for such a tax means those things have got to be removed. So now discounting a CGT and there’s a small gap there. Like the rains not going to gush in.

Compounding this is compensating beneficiaries because welfare is vary low with high penalties. Imagine accumulating $250 per week in emergency motel costs while receiving two hundred dollars benefits. So putting anything on this has far greater consequences to fiscal yields. The cost of compensating tax payers is far greater.

So the savings argument of which all the surpluses have been built since 1991 falls apart because the savers are all on higher incomes.

So if the tax working group doesn’t yield kindness we’ll all end up with wet shoes.

Sam

The TWG are not recommending GST goes down. Sadly they have not stood up to the government who took the family home off the table and disallowed any increased tax rate

Was lead to believe that the trade off for not taxing the family home was for existing houses only. I’m not sure how the TWG intend to cap CGT of the number of family homes. Just have to wait and see.

Going by the news, Qatar has opted out of OPEC by its own choice.

Saudi Arabians pay no taxes, it’s the greatest tax haven in the world but no one wants to live there. They’re not the most reliable neighbour going around. The greater the distance between Saudi and Qatar, the fewer the irainin missiles fall on Qatar when the poo poo hits the fan.

I remain convinced that almost the “whole” answer is a financial transaction tax on every dollar.

GST is a depressingly regressive tax (& there are many who are able to recoup that tax money, & it isn’t people like me – elderly, very unwell, still paying off a mortgage at nearly 80y.o. & & &. Being a retd. NZRN, I well know that EVERY SINGLE PHARMA DRUG IS A TOXIC, POISONOUS CHEMICAL, THAT ONLY SUPPRESSES SYPTOMS. There’s not one that cures/heals!

My costs have only increased; my superannuation minusculey increases each April, & won’t even buy a loaf of bread or some milk.

The likes of Susan St John would likely consider me to be wealthy. BUT my house needs all the spouting replaced. Dry rot both inside & outside needs cutting out & replaced with sound wood. I need a plumber to find a leak under the kitchen sink (don’t fret – I’ve SEARCHED for it.) I could go on but …

I’ve had to give up my St John alarm – at $725 + p.a. I simply couldn’t afford it anymore. People think I’d qualify for WINZ assistance. In my experience WINZ help the least possible: they’ve told me I’m getting the max I’m entitled to.

I live day & night with the pain & exhaustion that is greatly part of Multiple Sclerosis. I simply don’t have the energy to do battle with that loathsome organisation anymore!

No Isabel

I would not think you were in the top 20% of the wealth distribution.

the money from a net equity tax could be used to relieve some of the pressure you and others are under