GUEST BLOG EXCLUSIVE: Suzie Dawson – Kiwibank thumb their nose at the Banking Ombudsman

Last Friday, Kiwibank ‘debanked’ me, unceremoniously shutting down both my personal and business) accounts without so much as even a confirmation email. This is the latest blow in a long saga (detailed in my recent article “Kiwibank are breaking up with me“) where trying to liaise with the state institution has resulted in a litany of stonewalling and gaslighting and ultimately debanking.

The shock of this has been exacerbated by the realisation that it’s not just the ordinary customer on the receiving end of their disdain, it’s also evident in their dealings with the Banking Ombudsman’s office too.

Because of course, when it was clear that I was getting nowhere with complaining about Kiwibank to Kiwibank, I followed due process and went to the Office of the Banking Ombudsman. And the people there have been great to deal with. They are responsive, they are diligent. They took my case seriously, agreed to formally investigate it, held a meeting with us and truly heard out our concerns about the way we’d been treated by Kiwibank.

The Ombudsman’s representative was empathetic and attentive and worked with us to find potential ways to engage Kiwibank to resolve the issues that would de-escalate the situation. We left the meeting with a plan for a pathway forward for her to mediate with Kiwibank, and felt tentatively hopeful.

____________________________________________________________________

Where the story last left off, our accountant had written to Kiwibank requesting a 30 day extension of time before the debanking. From its past record of constant failures to respond to our communications, we were unsure if a response would be forthcoming at all. However, Kiwibank granted a 14 day reprieve and set a deadline of May 2nd, 2025.

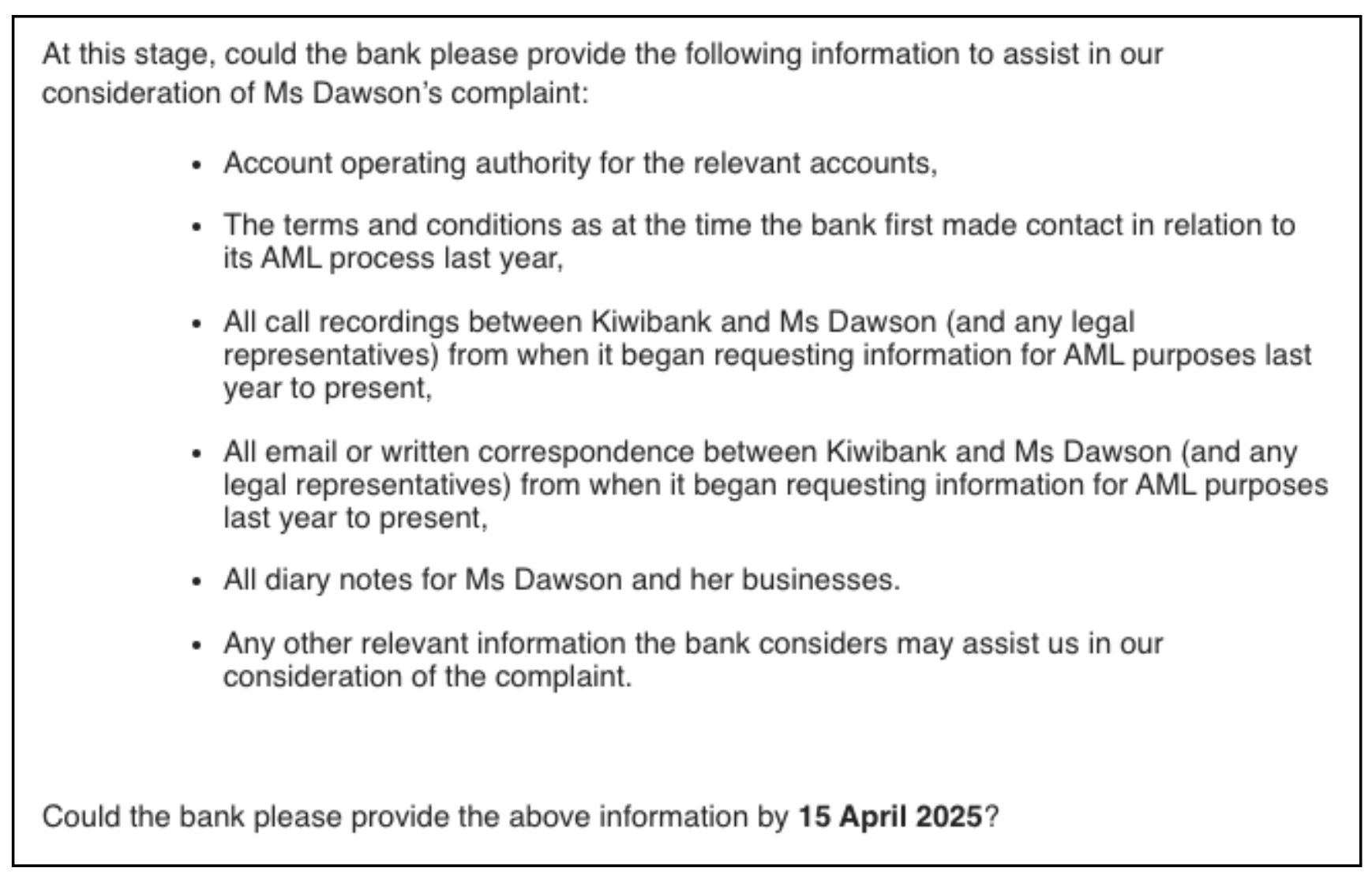

Meanwhile, just as they’d promised, the Banking Ombudsman’s Office acted swiftly to investigate our complaint. They set their own deadline for Kiwibank – April 15th.

By that date, Kiwibank were to provide them with the following information, outlined in an April 8th email from the Ombudsman’s office to the bank:

Subsequently, the bank requested an extension. In good faith, the Ombudsman’s Office duly granted it. The new deadline for Kiwibank to comply would be Tuesday, 29th April.

On Monday, 28th April the Ombudsman’s Office followed up on a meeting we had with them not long prior, confirming that they would request on our behalf that the bank provide an additional extension to the looming debanking deadline.

“In order to provide a reasonable opportunity to explore your case through the judicial system, while minimising impact to the business, you also request the bank provide a further extension of 6 months to keep the accounts open. As discussed, I’m happy to put this to the bank and will let you know when I hear back from them.”

And hereafter lies the problem. The Banking Ombudsman never did hear back from them. Strike 1.

The April 29th (extended) information deadline came and went with still nothing from the bank.

The Banking Ombudsman wrote to the bank again on April 30th and got no response. Strike 2.The Banking Ombudsman then wrote to Kiwibank’s “senior staff” on May 2nd, the bank’s stated deadline for account closing – no response. Strike 3.

But that same day – Kiwibank went ahead and closed the accounts.

It is one thing, as a customer on the downside of a power imbalance, to be abused by a state bank. But New Zealand is a democracy, and the strength of a democracy is reinforced by systems of accountability, transparency and the ability to gain redress.

So what happens when a state bank doesn’t even bother complying with – let alone respect, or fear – the very systems that exist to hold them to account? Systems directed by credentialed, educated, upstanding pillars of the community, appointed by government bodies acting in accordance with long-established legislation?

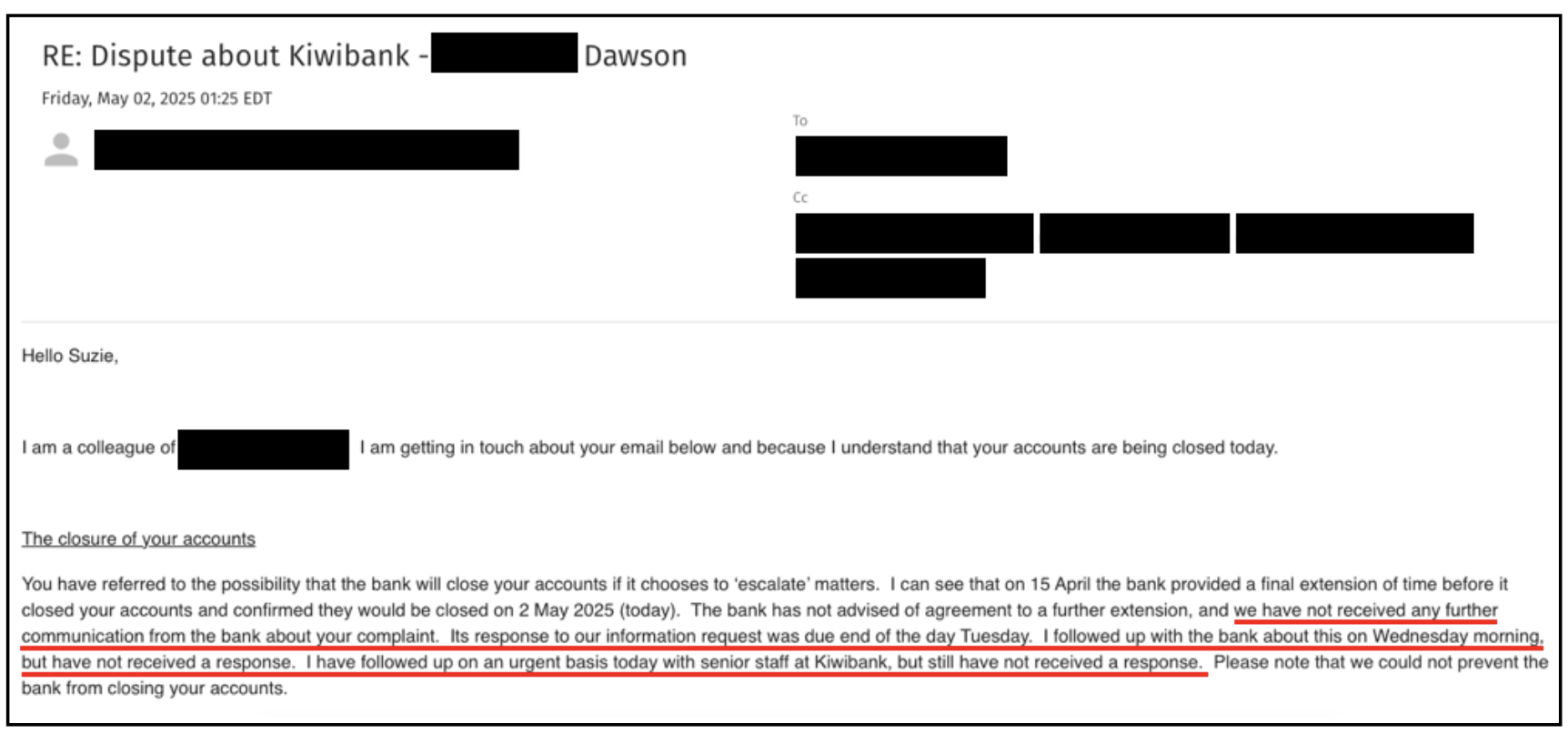

In the below email to us, dated Friday May 2nd, the same day as the accounts were closed, the Ombudsman’s Office transparently recounts the absence of engagement by the bank:

“…we have not received any further communication from the bank about your complaint. Its response to our information request was due end of the day Tuesday. I followed up with the bank about this on Wednesday morning, but have not received a response. I have followed up on an urgent basis today with senior staff at Kiwibank, but still have not received a response.”

It is now a full week later than the extended deadline for Kiwibank to provide the Ombudsman’s Office with the requested information and it’s still crickets from the bank.

How is it that a banking institution thinks they can thumb their nose at an Ombudsman’s office with impunity?

What’s the broader relevance of my case? If the Banking Ombudsman’s Office – an organisation led by people with letters like “CNZM” and “KC” after their name – cannot get a bank to answer their queries or to provide any information, then who on earth can?

How are us little people supposed to get any action on our complaints? We tried Kiwibank’s complaints department – that didn’t work. We tried requesting (time and again) mediation with Kiwibank – that didn’t work. We tried having the Banking Ombudsman’s Office investigate – that didn’t work. How could it be that that there is such a culture of wanton impunity in NZ’s flagship state banking institution?

____________________________________________________________________

Something just doesn’t add up. So I dusted off my old investigative journalist hat and started digging.

Step 1: Look at Kiwibank’s published disclosure documentation.

I read their legal disclosure statements – namely their General Disclosure Report, annual report/financial statements – something that only a former Financial Controller like myself could find interesting. That was an extremely long) read. While it taught me an immense amount about the tools that institutions of Kiwibank’s size use to justify their complicated accounting decisions, it didn’t resolve the issue at hand.

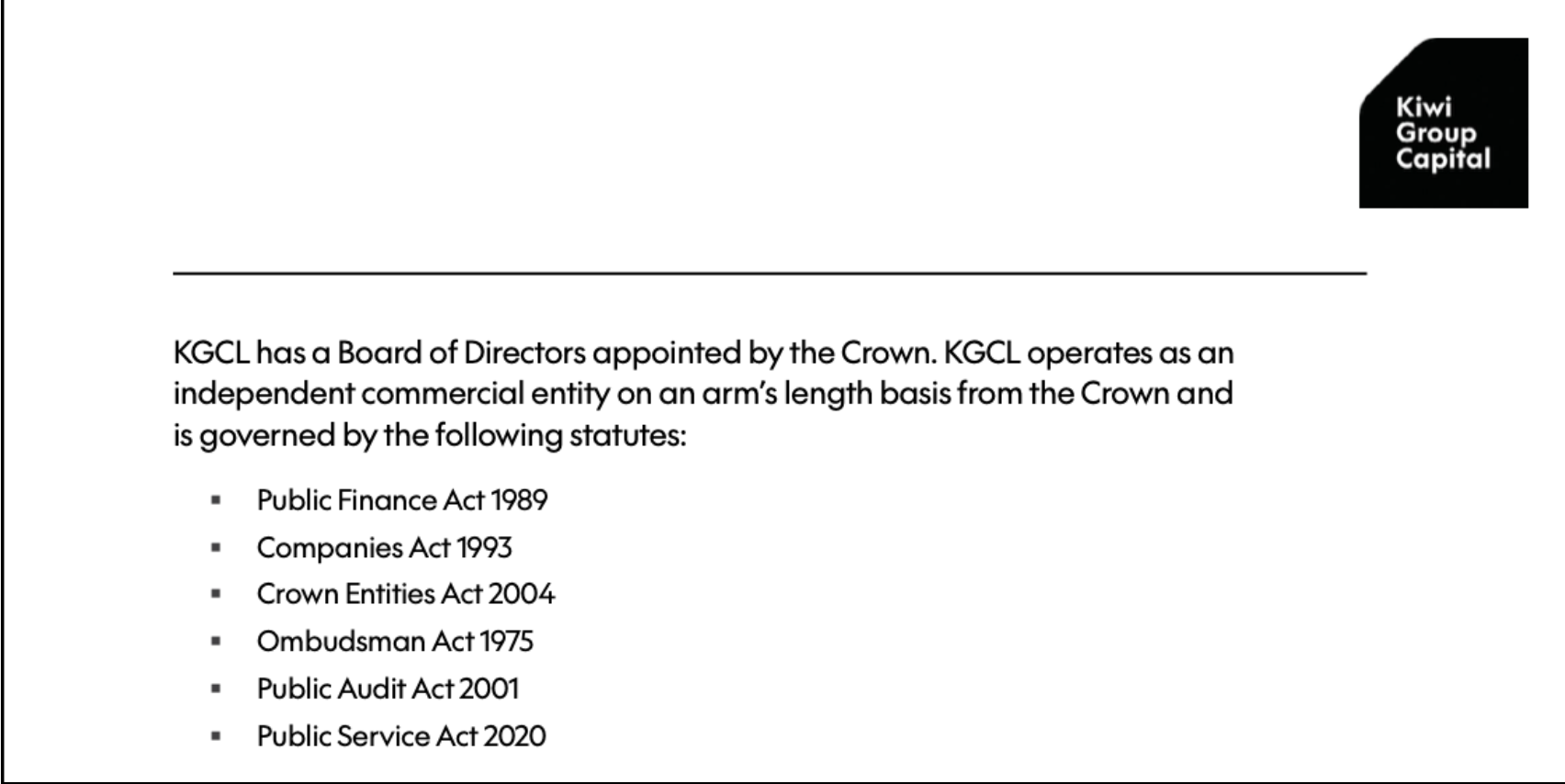

Until I landed at the Kiwi Group Capital Limited (KGCL) Statement of Intent for 2024-2027. That’s when puzzle pieces started falling into place.

KGCL is the holding company (the 100% owners) of Kiwibank and are in turn 100% owned by the Crown. The Crown appoints KGCL directors.

The document is packed with what in my case, turned out to be broken promises, like “Trusted – Kiwibank is a trusted bank – that delivers good customer outcomes every time” and “Empowered – Kiwibank takes ownership and acts quickly for its customers”.

But it is revealing: I discovered that KGCL is bound by a raft of legislation including the Ombudsman Act 1975.

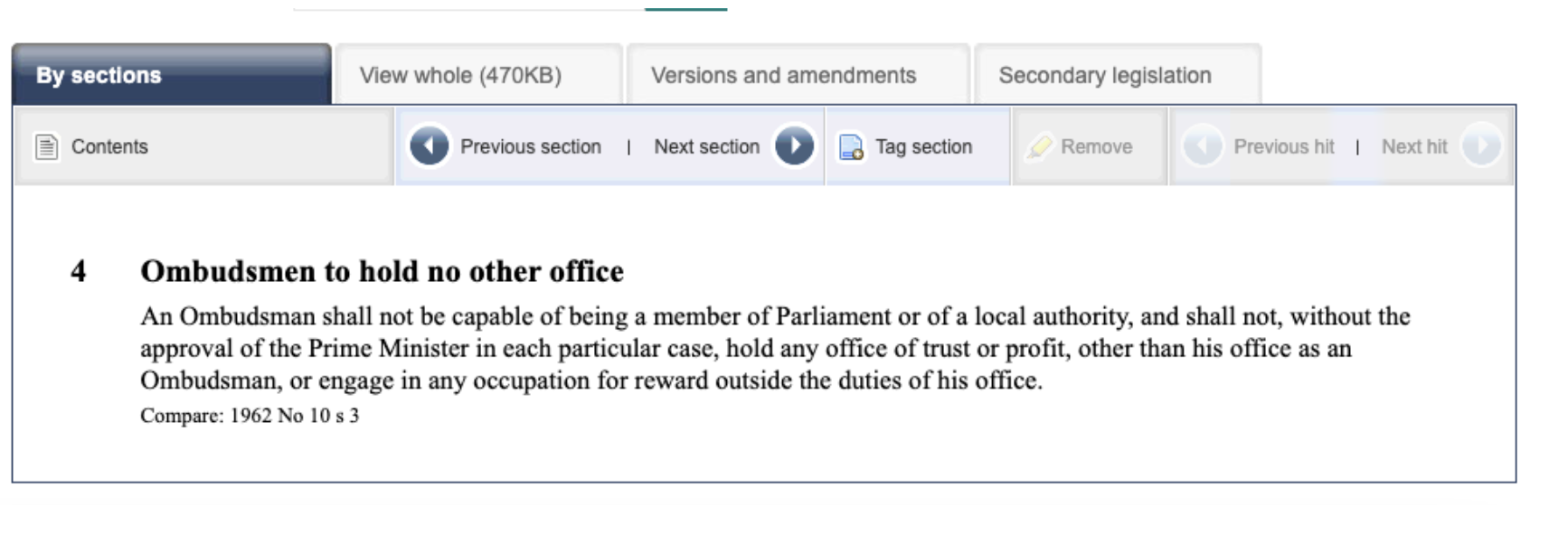

The Ombudsman Act 1975 exists to appoint the position and powers of a Chief Ombudsman appointed by the Governor General to provide (optimistically) independent checks and balances upon a wide variety of institutions and who oversees the various Ombudsmen underneath him.

Basically if you have a complaint about a public service – this is the top dog.

I looked up who the current Chief Ombudsmen is – it is John Allen.

It turns out to be an Ombudsman, you have to resign from everything else you do.

So what else has John Allen done? An enormous amount, and I won’t get into all of it here. But most pertinently, it turns out he was a Director of… wait for it… Kiwibank.

Three separate times in fact. And in one tenure, for six years.

This got me thinking about the Banking Ombudsman’s Office again. Why are they seen to be so toothless as to be able to be steamrolled by a bank they exist to provide oversight of? Who is on their board? Who are their Directors?

“The main function of our board is to ensure the independence of the Banking Ombudsman and to make sure that we are well-run and effective.“

So says the title print on the homepage of the Board of Directors of the Banking Ombudsmen’s Office.

Independence.

Effective.

The next discovery knocked my socks off.

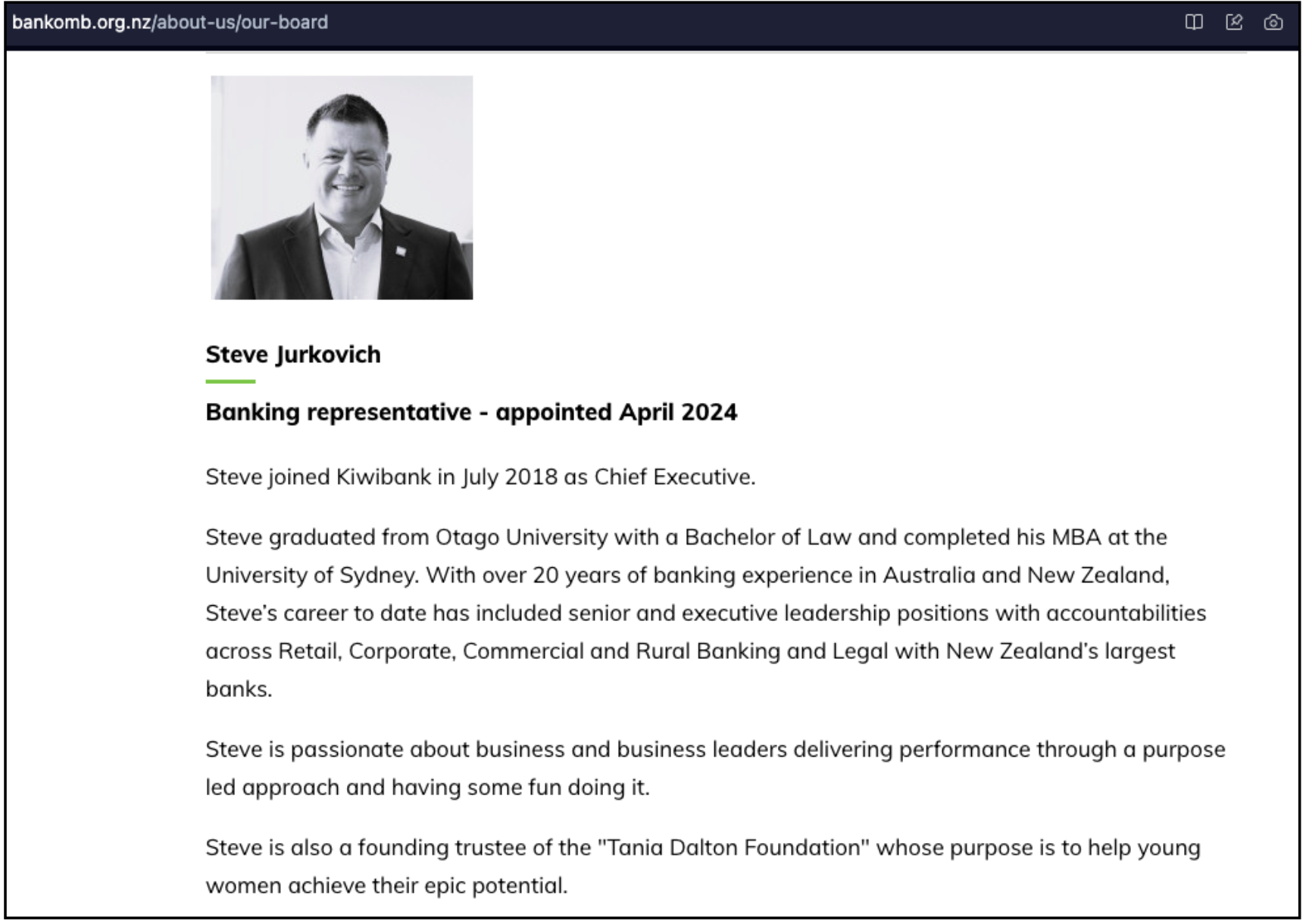

I scrolled through the page, reading the typically impressive bios of the Kiwi intelligentsia. Until I saw a name I instantly recognised and my jaw hit the floor.

OK, I thought. “Banking representative“. That sounds like an advisory thing right? Maybe he just gets consulted now and then on background or something? Maybe he’s at arms length from the board?

Nope.

Steipo Tony Jurkovich – apparently that’s “Steve” – is in fact a fully consented Director of “Banking Ombudsman Scheme Limited” the incorporated company of the Banking Ombudsman Scheme.

And why did I recognise him?

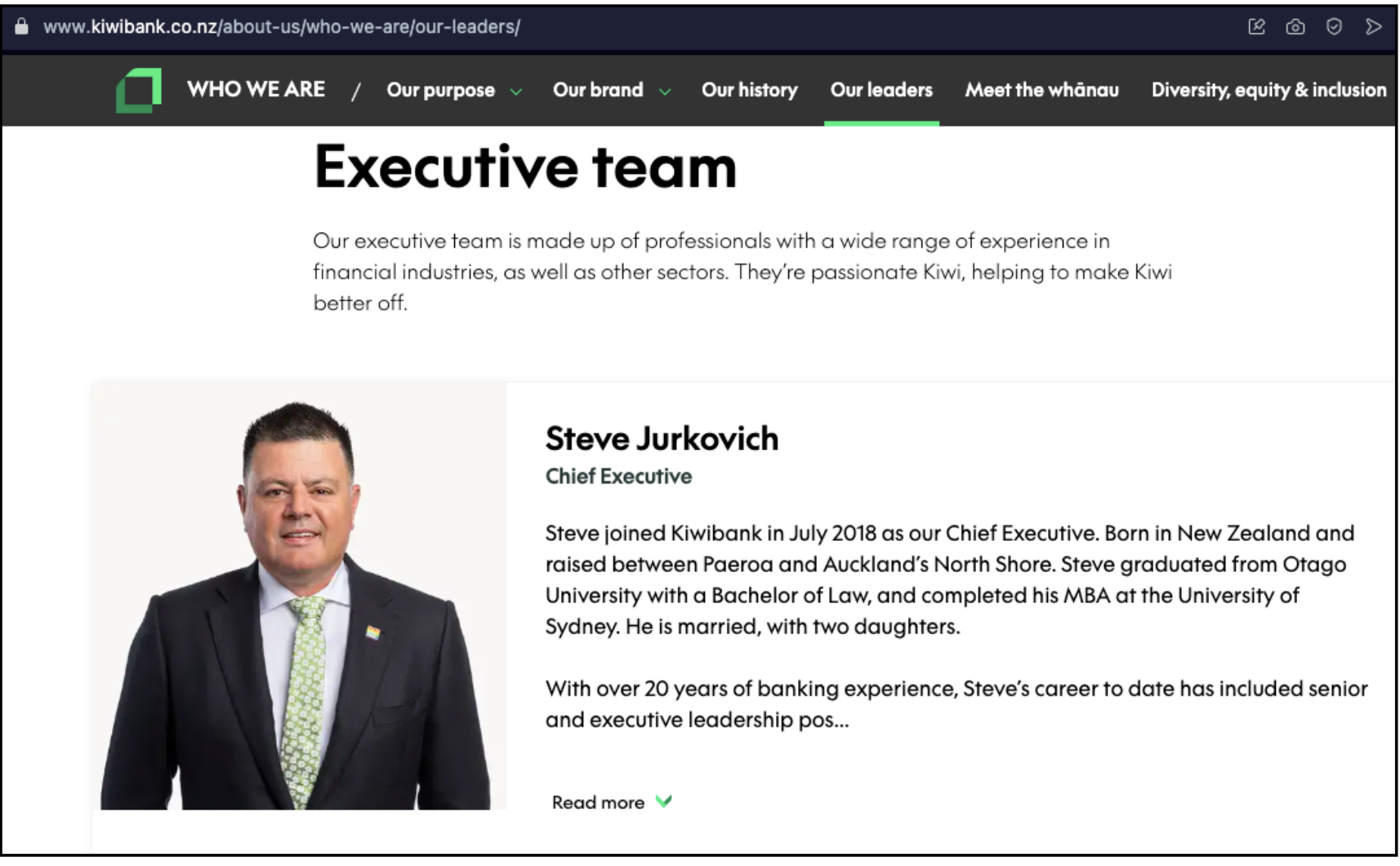

Because this is the Steve I’d seen on Kiwbank’s website:

How independent can an organisation be that has a Director who has a vested interest in a company being routinely investigated by it?

The irony is not lost on me that I’m complaining about Kiwibank to an Ombudsman directed by the CEO of Kiwibank and if I don’t like it, I can complain to a Chief Ombudsman who is an ex-Director of Kiwibank.

Is this why Kiwibank is just thumbing its nose at the Banking Ombudsman?

The Banking Ombudsman’s office is getting the same response from Kiwibank as I am – treated as if they were irrelevant, beneath notice, not worth bothering about.

And when push comes to shove – and Kiwibank just stonewalls them – there doesn’t appear to be any meaningful recourse at all.

For the Banking Ombudsman’s Office to truly be “independent” and “effective”, there’s going to have to be substantial change.

Just as with Kiwibank, it is abundantly clear to me that the problem isn’t at the bottom – it’s at the top.

____________________________________________________________________

According to the 2022 Annual Report of the Banking Ombudsman, of 4,732 inquiries that year and 3,131 complaints laid, only 4% of complaints failed to achieve “early resolution”.

It appears I’m one of the proverbial 4%.

Debanking – a crippling punishment that renders you unable to access fundamental utilities required for participation in modern life – is becoming a bigger issue by the day. In our Bad Banki campaign (which I wrote about previously) we have been tracking global media stories about this issue.

The numbers involved are staggering. 4.6 million Suspicious Activity Reports in the UK alone: 500,000 customers debanked.

The US and UK are moving swiftly to limit or end the practice. New Zealand must do the same.

New Zealand First have tabled “The Financial Markets (Conduct of Institutions) Amendment (Duty to Provide Financial Services) Amendment Bill” to address debanking, but have pitched the issue as being the political right being persecuted by the political “woke” left.

The debanking of myself and my businesses proves that debanking is not targeted at only one side of the aisle. It is in fact a pincer – and like all abuses of power, it starts at the outer edges, but will inevitably squeeze into the middle.

If something isn’t done about this and swiftly, it will not be long before your “issue-motivated group”, your charity, your church, your union, your employer, your sister or brother or cousin feels the cold touch of an industry so incestuous that it sits in seats of power on its own regulating boards while refusing to comply with them.With conflicts of interest this naked and rife, why bother even calling ourselves a democracy at all.

__________________________

Suzie Dawson is a former activist, journalist and political influencer now Founder and Chief Product Officer of privacy-respecting software development house Talk Liberation Limited “

Media enquires: media@talkliberation.com

Thanks for sharing your experience, Suzie. It raises important questions about how ‘debanking’ can be used against people who challenge the status quo.

Yep, unless Kiwi Bank respond and come clean,…… fk you, I’m out as well.

It’s like having bank robbers investigate themselves and expecting this to show some form of justice.

Absolutely vile. There is no sense in having a ‘New Zealand bank’ when it is completely within the claws of the same usurers who make the ‘Australian’ banks evil.

“We have investigated ourselves and we have done nothing wrong!” – Kiwibank 😀