GUEST BLOG EXCLUSIVE: Suzie Dawson – Kiwibank is breaking up with me

After a 25-year love affair, Kiwibank is breaking up with me.

I owe them nothing. No debt whatsoever. They make money out of me -I don’t take any form of funding from them.

The money that moves through my accounts is my own – not theirs.

My accounts with them are managed by the NZ-based FCPA (that’s a super qualified accountant) of my group of businesses.

I have happily paid enormous amounts of tax in New Zealand and everything is done by the book in our businesses, and yet in March, Kiwibank sent Dear John letters not only to myself, but also to my accountant, and to the co-Director of my NZ business (an upstanding career CEO who has led major NZ companies including a public company) to let us know Kiwibank is breaking up with all of us.

This hurts morally even more than it does financially – I have supported Kiwibank relentlessly since its inception.

I prided myself on the “Foundation Customer” stamp on my ATM card. I lobbied my friends and family across years, to move their banking to Kiwibank and to support it.

I thought what Jim Anderton did for New Zealand was incredibly important – I believe in state-owned enterprise.

When the state owns enterprises, they turn profits which offset the burden on taxpayers and strengthen the nation.

When the government of the day comes along and fire-sales state assets to industry, the strategic outcome for both the economy and also for ordinary people is always worse.

It is a pity and a shame. But I digress. Back to the break-up.

__________________________________________________________

In Martyn Bradbury’s recent editorial about this case, he mentioned the first time Kiwibank attempted to de-bank me – it was in the direct wake of 2014, the most politically turbulent year of my past activism and journalism. (Yes, the year of Dirty Politics but also of #NZ4Gaza, #TPPANoWay and the Moment of Truth.)Kiwibank didn’t substantiate or provide any cohesive reason for the attempted closure, and after the intervention of my lawyer, Kiwibank backed down and allowed me to keep my accounts.

Similarly, their account closure notice of March 20, 2025 does not sufficiently explain the reasons for their actions. It states only:

“As a financial institution, Kiwibank is committed to complying with all applicable legal requirements, including those related to anti-money laundering and sanctions. Following a risk assessment, we regret to inform you that we are unable to continue providing banking services to you.“

What money-laundering? What sanctions? I have never been paid a single rouble the entire time I have been in Russia. 100% of my income has been earned outside of Russia, declared in New Zealand and my tax paid in New Zealand. My businesses are legitimate, our sources of income are legitimate. In Kiwibank’s methods of closing my accounts, we are accused without being accused – kept in the dark and not allowed to know the real reasons ‘why’.

The lead-up to the current de-banking attempt seems to be “enhanced due diligence” checks initiated by Kiwibank in 2023. This despite the fact that Kiwibank had already been transacting from NZ to Russia on my behalf for some 7-8 years prior, without any apparent issue, and while raking in substantial fees on each transaction in the process.

It certainly wasn’t the Russia-Ukraine war that triggered this: February 24th 2022 and the implementation of sanctions came and went without any disruption of service.

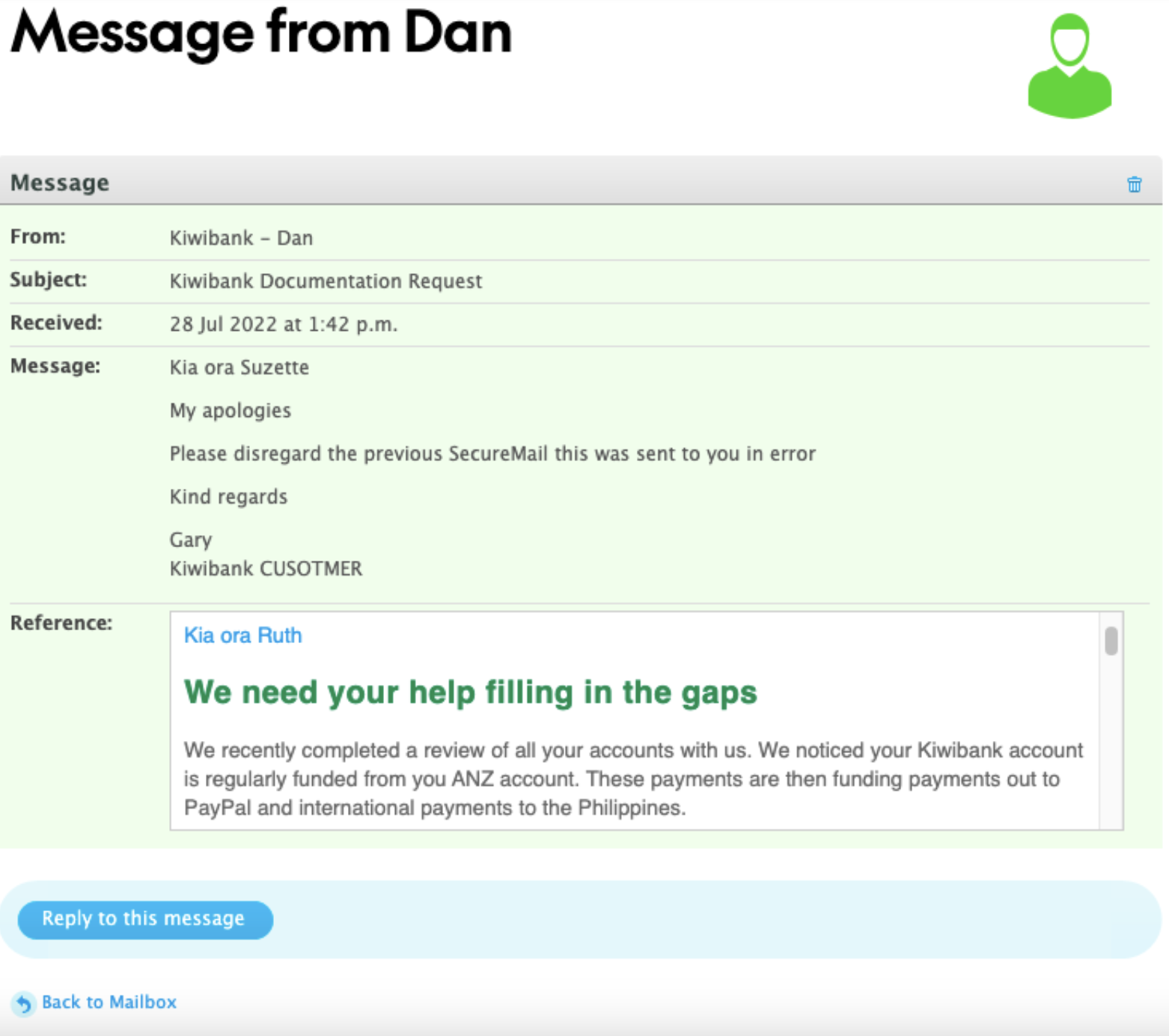

However, in July of 2022 alarm bells did start ringing for me when Kiwibank’s “Customer Verification Team” sent me a “SecureMail” inside Kiwibank’s internet banking platform about AML checks.

They called me “Ruth”, asked me about my ANZ account and my transactions to the Philippines. They supplied a case file number which I won’t publish here for obvious reasons.

The problem: my name isn’t Ruth, I don’t have an ANZ account and I had not transacted to the Philippines.

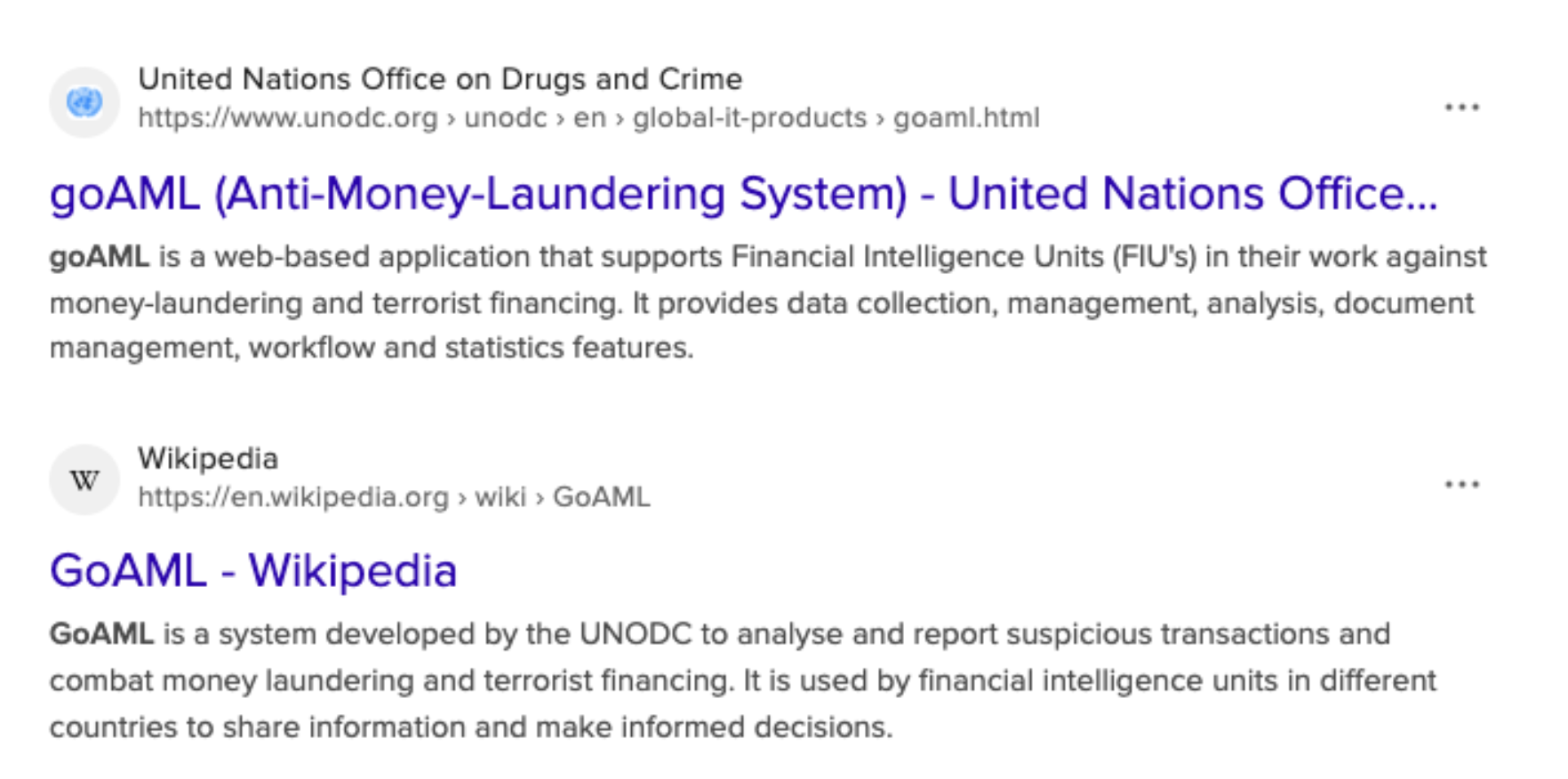

The implications of this are obviously a privacy nightmare. The AML system – known as “GoAML” internationally, and to which New Zealand’s financial, legal and other institutions subscribe and use – is chock full of highly sensitive and private, supposedly locked down, information accessed by NZ Police, Financial Intelligence Units, government departments and even our nation’s esteemed spy agencies, the NZSIS and GCSB. The secure nature of the use of the platform is a legislative requirement.

Ruth starting with an “R” and my name starting with an “S” could well be a coincidence. But in order for the mix up to occur at all, my software analyst background told me that there had to have also been an AML case file about me open in the background – one which I had not been made aware of the existence of. Only this would have enabled a “mis-click” to occur – where the wrong line of a dropdown or a data table was selected by a sloppy employee working with insufficient checks and balances before hitting ‘Send’, causing me to wrongfully receive Ruth’s private information.

Somewhere out there, was Ruth reading my personal information in her Kiwibank internet banking “Securemail” system? Or another customer’s?

It’s entirely possible, but I don’t know.

Kiwibank said sorry, and nothing more was made of it. And I didn’t hear anything more from Kiwibank at all about AML for a full year.

Fast-forward to July 2023 and there it was: an email containing the invocation of “enhanced due diligence” – which under the legislation, euphemistically enables collection methods up to and including spying.

Invasive, comprehensive, deep dives by all available means and methods, into the life of a target – in this case, me.

We complied. As we always have. My accountant and lawyer and I provided every document asked of us, fulfilled every information request.

And after a month, the verdict from a Kiwibank AML team manager came down:

“I can confirm, the information you have provided has satisfied our obligations, where the need for Enhanced Due Diligence (EDD) was required.“

OK, we thought. That was easy. All we have to do is turn our lives upside down for these people and everything will be fine. Onwards and forwards.

__________________________________________________________

Founded in 2021, our privacy-focused software development house is called Talk Liberation: https://talkliberation.com.

Our mission is best summed up in one simple phrase: “Your data is valuable. That’s why we don’t collect it.”

You can find out more about us at our Press Page: https://panquake.com/press

We are the creators of the upcoming Panquake social network: https://panquake.com

Thanks to a viral crowdfunding campaign – without any institutional funding or backing – we attracted more than 3 million visitors and 3,800 donations from regular people, and later, support from private investors impressed by the prototype software we built.

About 18 months ago, we released Panquake Me, a FREE link shortening, cleaning (no trackers or cookies!) & archiving service.

We will soon release Lnqk Me (pronounced Link Me) which is a privacy-respecting digital marketing dashboard for anonymously tracking digital marketing metrics while protecting your audience and yourself.

We also created and released WLDragnet.com which exposed the drag-netting of tens of thousands of Twitter users for political targeting by US defence contractors.

Each of our websites has a FAQ page that explains more about each project.

CIA torture whistleblower and New York Times best selling author John Kiriakou is the Brand Ambassador for Talk Liberation and our Media Director is journalist and influencer Fiorella Isabel from “The Convo Couch” fame.

From our humble beginnings as a project staffed by volunteers who just wanted to create software that you can use without your data being abused, we now have global operations, with nearly 50 team members in more than 14 countries.

Thanks to our intensive labour and our refusal to give up, we have grown exponentially year on year, despite the pushback we have faced. We now have dozens of developers working around the clock and around the world, on multiple different projects and products.

We are a Kiwi tech success story in the making. The kind of which Kiwibank should be proud.

And this is just the beginning.

__________________________________________________________

It is difficult to know which came first: the chicken or the egg.

In September of 2022, our USD$1 million seed funding was frozen without notice and withheld from us, by Islandsbanki, a major Icelandic bank. Talk Liberation’s data operations and hosting are in Iceland, because Iceland has special constitutional protections for freedom of information and freedom of speech, and data centres in Iceland are powered by 100% green, renewable geothermal and hydroelectric energy.

The bank invoked “anti-money laundering and counter terrorist-funding” legislation to justify the freezing, and then closed our accounts. But then, in a stunning reversal, they unfroze our funds – but without apology, explanation or compensation. Of course, the unfreezing of the funds completely exonerated us from wrongdoing. But it was too late – the damage was already done. Strategic plans that we had spent months working on had gone out the window – hiring couldn’t proceed, strategic partnerships had to be delayed. And our community suffered fear, uncertainty and doubt as time ticked on.

In March of 2023, we began preparing a legal case against the bank.

While we don’t question the rights of banks to freeze funds in certain circumstances, we absolutely are requiring that they be held to account for the abuses of process that occurred, the lack of transparency or customer care and for the damages and costs that were inflicted upon our business.

It was ultimately nine months before we received our investment funds back.

Our lawsuit is progressing with the help of Icelandic lawyers who won a USD$10 million settlement for WikiLeaks against a payment processor acting on instructions from Visa and Mastercard. With their help, we are currently suing Islandsbanki in Icelandic Courts for wrongfully withholding our investment funds. More info about that can be found here: https://badbanki.com

The process of freezing our funds in Iceland would have involved the bank filing a Suspicious Activity Report (SAR) in the global financial intelligence system. Such a report, about a New Zealand business owner, would travel via FIU-ICE (the Icelandic Financial Intelligence Unit) to the NZFIU (New Zealand’s Financial Intelligence Unit). And vice versa.

We have no ability – at least yet – to learn the contents of those reports, what allegations were made about us, or what their impacts were. Because we can’t see them, we can’t correct them if they contain false or misleading information.

We know that AML legislation empowers those reports to be transmitted to financial entities which have ‘shared customers’. In this case, such as Kiwibank.

The AML system itself is a siloed black hole filled with personal data that is coupled with ‘suspicion’ and ripe for abuse by any institution or bank employee who decides they don’t like someone, for whatever reason.

The damage a wrongful or malicious report can cause, is literally global.

So we are left wondering – was Kiwibank the chicken? Or was Islandsbanki the chicken – and is Kiwibank the egg?

__________________________________________________________

One of the most famous whistleblowers in history told me many times “The spies are the banks. The banks are the spies”. I was dubious and perhaps naive at the time – but I now understand firsthand exactly what they were trying to tell me about.

And there is one thing I do know.

I’m sick of being spied on, people. As a single mother from Birkdale it is absolutely ludicrous that I was targeted for surveillance and extrajudicial punishment just because I dared to participate in (supposedly democratically-protected) social movements in New Zealand.

And I don’t like you all being spied on by default either. (That’s what mass surveillance is. Spying by default.)

Not only is it an immoral violation of privacy – it’s a violation of everything from the Bill of Rights to the United Nations Covenant on Political and Civil Rights to a half dozen other agreements to which NZ is a signatory. Our populations are not supposed to be spied on – and reported on – wholesale. It is not what we were promised when our societies were established, nor our international relationships.

In terms of what the banks are doing to us right now, it is also a violation of economic freedoms. Iceland is ranked number 11 in the world for economic freedoms. New Zealand is ranked number 3.

Economic freedoms are similarly enshrined in international law. Such as the International Covenant on Economic, Social and Cultural Rights (which New Zealand and Iceland both signed in 1968 and ratified in 1978 and 1979 respectively.)

In those laws and principles, there is a higher onus on state banking institutions to both provide methods of redress and to apply resource to assuring the rights of customers.

According to slide 12 of the OHCHR’s ‘Guiding Principles on Business and Human Rights’:

“Where States own or control business enterprises, they have greatest means within their powers to ensure that relevant policies, legislation and regulations regarding respect for human rights are implemented.”

Economic freedoms including specifically those related to entrepreneurship are widely considered by experts to be inherently interlinked with political freedoms. One cannot exist without the other.

Quoting now from Wikipedia’s article on Economic Freedom:

“Some free market advocates argue that political and civil liberties have simultaneously expanded with market-based economies, and present empirical evidence to support the claim that economic and political freedoms are linked.[24][25] In Capitalism and Freedom (1962), Friedman further developed Friedrich Hayek’s argument that economic freedom, while itself an extremely important component of total freedom, is also a necessary condition for political freedom. He commented that centralized control of economic activities was always accompanied with political repression.”

What that means is that one of the very justifications for our modern financial system in capitalist societies is that it empowers political freedoms and thereby democratic rights.

But abuse within these systems and the increased centralisation of control mechanisms is now endangering both economic and thus political freedoms. And the result is, as Friedman prophesied, political repression.

__________________________________________________________

Our founding democratic legal frameworks and international law itself is laying in tatters around our feet because too many people feel paralysed by fear and helplessness to do anything about it.

What dismays me most is those who have been conditioned to accept it.

To accept the crimes, and to cower before the criminals who mouth ‘democracy’ while flouting democracy, every single day.

It is unfortunately true that if you stand up, you might end up like me.

Or like Ed. Or like Julian. Or like Kim. Or like Roger Ver.

But in all those cases – we aren’t just cautionary tales. We are builders.

We are doers. We create things. Things that were and are an important part of the pushback that protects all of you and that creates a better society.

Kim’s Mega benefitted users, regardless of the systemic interference he has faced. WikiLeaks benefitted the public greatly – WikiLeaks files have been successfully referenced in and thus transformed the outcomes of tens of thousands of court cases. Ed’s Freedom of the Press foundation benefits journalists and a free press. Roger Ver’s first forking of Bitcoin to create Bitcoin Cash benefited countless small retailers predominantly across Asia but in other places as well, and set a precedent that Ethereum and countless others followed to create space for enormous diversity and innovation in the blockchain industry.

All of the people I have named paid a massive price, because all of them were making an enormous contribution.

That’s why all of them deserve your support.

You can argue flaws in all of these people or the organisations they created and that’s easy to do, because they are humans, doing the best they can under incredibly trying circumstances in which there is no “How To Be The Perfect Dissident Innovator” guide book to follow.

But if you’re critiquing them you’re looking in the wrong direction. You’re ignoring the elephant in the room. To the detriment of yourself, your families, your neighbours, your grandkids and great grandkids.

__________________________________________________________

I never thought I would have anything in common with Gloriavale.

A closed sect of fundamentalist Christians, like many communes, they’ve been plagued with sexual assault and slavery claims against women and children which would make your stomach churn to read about.

Yet somehow, I now discover that despite Gloriavale’s leaders being the literal ideological opposite of everything I believe, we mortifyingly have one thing in common: we have both been de-banked.

Which makes me wonder – if I, a leftist activist and journalist, and they – a far right fundamentalist Christian cult, can be meted out exactly the same treatment by banks – what is next for all you people in the middle of us?

According to data released by the Financial Conduct Authority, apparently as many as 500,000 customers in the United Kingdom were de-banked in 2024.

4.6 million Suspicious Activity Reports (SARs) were lodged – this is a nearly 20-fold increase from a decade earlier.

I could make some pretty graphs but do I really need to? The trend is obvious. More suspicion, more reports, and unjustifiable quantities of bank account closures.

So why is this happening?

It seems there are a few reasons. Let’s take the side of the banks for a moment.

The bank’s suspicious transaction automated detection systems are on a 24/7 rampage and are nowhere near as discerning as they would ideally be. I got a taste of this in 2020, during Covid, when my Kiwibank debit card was shut off because I had made an NZ$15 donation to a Buddhist retreat centre.

The system deemed it ‘suspicious’ and voila, my children and I found ourselves on lockdown with no access to funds.

In long back and forth exchanges, the bank told me they couldn’t possibly have the resource to have humans examine the accounts of every suspicious transaction.

4.6 million suspicious activity reports would logically mean 4.6 million investigations. Investigations are expensive. Therefore accounts that trigger automated suspicious activity reports are expensive.

Banks can’t simultaneously please legislators and satiate the requirements of reporting authorities without it eating into their profits.

But the increasing rates at which customers are being de-banked is simply unsustainable.

At the current trajectory, an ever increasing sector of society will find themselves without a bank and therefore unable to function in the modern world. That will lead to them using friends or families accounts, or other workarounds, which will in turn trigger more violations of banking policies and more suspicious transaction reports.

You can’t have both a cashless society and a society where a percentage of the population isn’t allowed to digitally transact. These goals are in tension with each other.

Now – do I think Gloriavale was de-banked because of automated systems? No. Nor do I think that I was.

We were ostensibly de-banked because of ‘risk’ management – and depending upon your perspective, almost anything can be assessed to be a risk.

Reputational risk or harm is something that Kiwibank is obsessed with. I know this, because when I once, years ago, tweeted frustration with them about some issue, my phone rang within the hour. On a Sunday afternoon.

Kiwibank’s call centres aren’t even open on a Sunday – if you are a customer and want help on the weekend you can forget it. But there was their emergency comms team making an unsolicited call to my mobile phone to ask me outright to please not tweet about them.

So being in Russia may be a ‘risk’ – but not just because there was a war, or because of sanctions. It’s a risk because when you need a $500,000,000 cash injection from private equity, you need to ‘de-risk’ to the maximum extent possible to secure your funding.

The great irony is that for all Kiwibank’s ‘risk assessment’ they failed to foresee the actual blowback that they are now creating with their actions.

When spies abused their powers against me, I became an expert in state surveillance and dedicated my life to educating the public about it.

Now that banks are doing it, I am studying AML legislation, frameworks and software and dedicating my life to educating the public about it.

I have no doubt that whatever craven violations of privacy the banks have squirrelled away in their precious Secret Squirrel databases may be weaponised to prevent us prevailing in Court. That isn’t a reason not to fight these abusive processes anyway.

Regardless of whether I am able to achieve justice for me, or for those around me who Kiwibank is rendering collateral damage, I will still fight for justice for all of you, fellow Kiwis. And thereby hopefully prevent you being de-banked before it happens.

To that end, I have instructed my team in the creation of a new public campaign that will specifically raise awareness about Kiwibank’s de-banking proclivities, and will search out other Kiwis who have already been in my shoes, or are about to be, but who may have less resource than I to do something about it.

The campaign will have an unforgettable name and we will announce the launch on The Daily Blog.

We will activate, we will educate, we will advocate, we will litigate and together, we will seek change.

Because human beings are more than the next “suspicious activity report”, economic and political freedoms are non-negotiable and banks must learn to be responsive to the rights of their customers.

__________________________________________________________

The timeline of communications between ourselves and Kiwibank reveals a Shakespearean tragedy of comical proportions on their part.

It would be even funnier if I didn’t have to pay thousands of dollars in legal and accounting fees for all of it.

You see – getting to the crescendo of the breakup – by the time July 2024 rolled around, Kiwibank were back for their next round of “enhanced due diligence” measures – and this time even more aggressively than the last.

Our company was growing – fast – and I was way past being able to rip myself away from developers and product deliveries to spend my time dealing with this or that information request. That’s what businesses have accountants and lawyers for, after all. In January of 2024 our FPCA had been added as an account authority, so surely he could deal with it on our behalf. Right?

Wrong. Despite having added him as an account authority themselves, Kiwibank failed to recognise that fact and refused to work with him.

They pursued close to 20 information requests, including demanding income statements for monies received from “Dreamboat.”

It took us a while to work out that what they actually meant was “Dreamhost” – a common web hosting provider, a supplier of services. Dreamhost had never paid me any money whatsoever. So there was no documentation I could provide no matter how much I wanted to comply.Kiwibank’s communications were frankly schizophrenic – they went from claiming it was about source of funds, to claiming it wasn’t about source of funds.

They demanded to know why I am banking with them – when I’ve been banking with them for a quarter of a century.

They demanded I supply documentation I had already supplied.

They demanded information which was literally visible inside the Kiwibank internet banking app itself. As if they had no idea what information their own systems contained.

“Please provide the following ID/information for both your personal and business accounts by 30/08/2024 or we’ll need to freeze the account(s) – this means no-one will be able to access them until we receive your ID/information, and on 01/10/2024 we’ll have to close your account(s) without further notice.”

Kiwibank already had a certified copy of my ID on record already, which hadn’t expired, but they wanted it again anyway.

I count 25 emails from my lawyer dealing with Kiwibank AML-related matters – both with Kiwibank directly and with myself – just in the period between July 2nd and September 4th, 2024, when Kiwibank confirmed a (revised) date for a break-up:

“In order to progress this further, can you please supply the following (nothing (sic) that on 1 October 2024 the account will be frozen and on 1 November 2024 the account will be closed).”

About a third of those 25 emails are us begging for them to respond to our prior emails. The reason the deadline shifted from 30 August 2024 to 1 October 2024 was because my lawyer pointed out to them that the first response we had received to any of our emails was on the very day of expiry of their self-imposed deadline. Making it impossible for us to comply within the parameters of their requests.

So – circling back to those hallowed international legal and governance principles for state institutions – what did Kiwibank’s “methods of redress” and application of resources to “assuring the rights of customers” look like? When we filed a complaint with the Kiwibank Complaints team, we got a response.

Six months later.

Our September 2024 complaint to the Banking Ombudsman tells the story:

* Kiwibank refuse to engage in reasonable and rational two-way communication with us, often completely ignoring our questions, requests or comments

* Kiwibank refuse to engage with the registered account authority (who happens to be a CPA no less)

* Kiwibank request information which they already possess

* Kiwibank make nonsensical information requests

* Kiwibank began this process by claiming it was about source of funds and then midway switched to claiming it wasn’t about source of funds

* Kiwibank, by their silence, persistently refuse to, (or unnecessarily delay) assign an account manager that could provide closer scrutiny despite repeated requests from us to do so, which is clearly a demonstration of goodwill on our part

* Kiwibank depersonalise their responses – we have gone from dealing with a named respondent to now receiving emails with no contact details at all that simply sign themselves “Customer Verification” – are we being answered by AI? Is this why nothing makes sense? Are we talking to a computer and not a person?

* Kiwibank are constantly changing the ballpark / goalpost lines on what information they require

*Kiwibank are now requesting information about transactions not relevant to the stated period, and which are within a prior period for which they already accepted our due diligence documentation as being satisfactory

The Banking Ombudsman, by comparison, responded to us the same day that we made a complaint.

They promptly contacted Kiwibank, and urged them to engage with us.

Thus, the Kiwibank tone softened. And they decided to give themselves an extension on their own (yet another newly revised) deadline.

“We are still currently reviewing your documents. Because of this, we have changed the account freeze date to 15th October 2024.“

We waited with bated breath until the fated day of the third Kiwibank-imposed deadline arrived.

And nothing happened.

It was crickets from the bank.We continued to transact as normal and heard nothing further.

Fast-forward another 6 weeks, and December 10th brought a lovely surprise: a random email from Kiwibank.

“We apologize for the delay in our response. We are currently reviewing our High-Risk Jurisdiction (HRJ) policy, which includes reviewing our customers who reside in HRJ’s. We hope to have this review completed and provide you with a formal response as soon as possible.”

So, in a nutshell, after blowing their own third deadline, and with the attention of the Ombudsman already on them, Kiwibank had decided that maybe their policies were insufficient to do whatever they wanted to do to me and to get away with it.

It was crickets again for more than a month: then Kiwibank sent us a customer satisfaction survey.

“For us, it’s a chance to listen and grow. For you, it could be a chance to help shape the future of financial services.”

And then there was absolutely nothing further until March 19, 2025, when out of the blue arrived:

“Kiwibank has decided it is no longer prepared to offer you banking services. Please see attached a closure letter for further information. We do not make these decisions lightly, and apologise for any inconvenience.”

What do you do at this point? Do you laugh? Do you cry?

The ineptitude and complete lack of introspection by the bank as to its own (mis)conduct defies all logic.

Of course – we protested the closure. My accountant, my lawyer and myself all wrote to the bank explaining how unnecessary and damaging the situation was, to no avail. We again contacted the Banking Ombudsman to follow up, and they again responded promptly and engaged with the bank on our behalf.

And yet again we wrote to the Kiwibank Complaints team – the same Complaints team that had never resolved the original complaint of six months earlier – who assured us that they would “start investigating your complaint“.

On March 30th, 2025 the hammer came down from the Complaints team:

“Whilst Kiwibank understand the inconvenience this has caused we will not be reviewing this decision. Kiwibank has now fully considered your complaint and this is our final position.”

In a final sick and ironic twist, the last lines of the email from the Complaints Team was to suggest that if we had a problem with it, we could complain to the Banking Ombudsman.

“If you remain dissatisfied, you can ask the Banking Ombudsman Scheme to consider your complaint and our response to it.”

The same Banking Ombudsman who had been engaging with Kiwibank on our behalf for half a year and counting.

__________________________________________________________

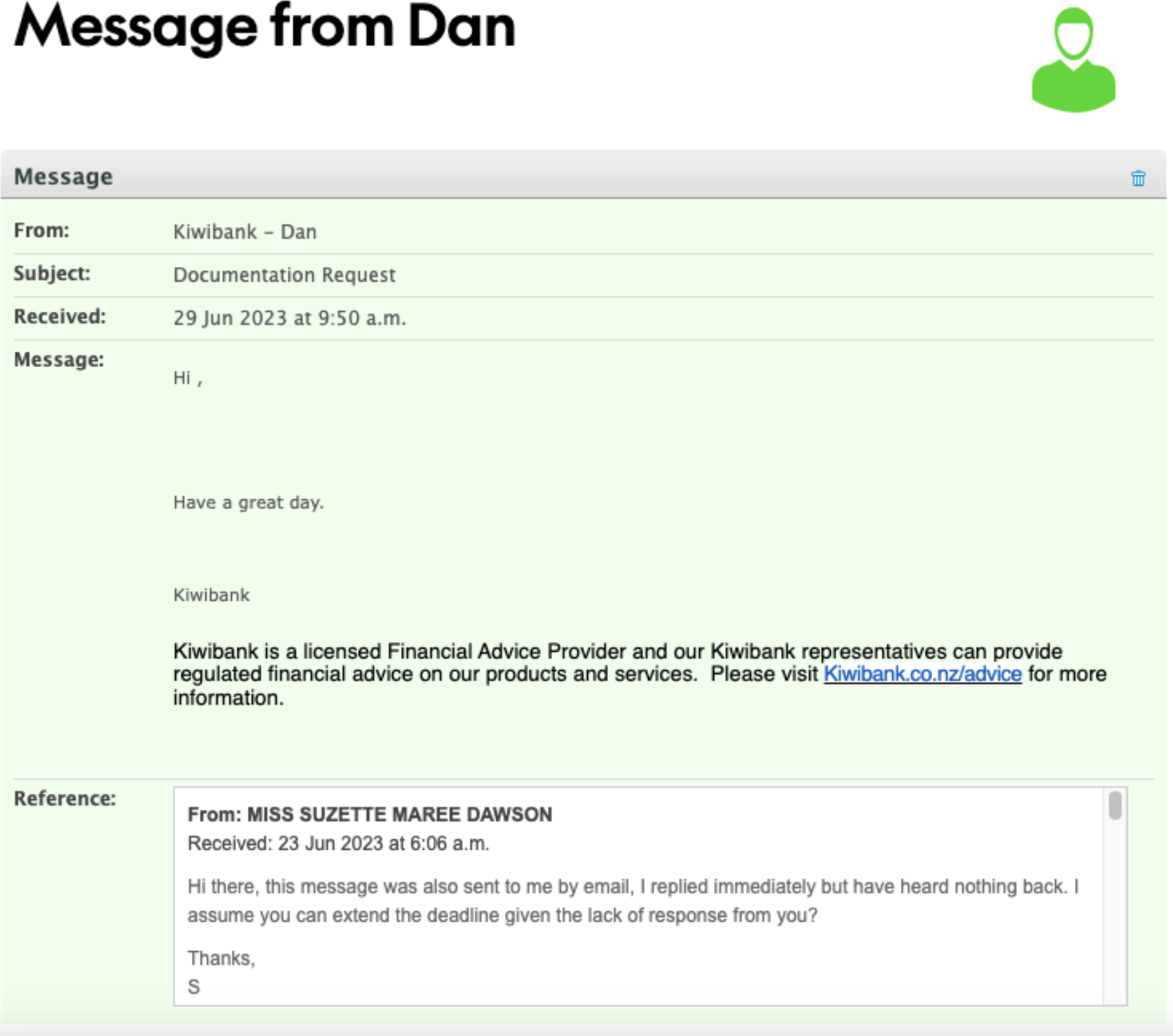

If I could sum up my experiences with Kiwibank in one screenshot, it would be this gem from 2023.

Our accountant has written to the bank and requested an extension to the deadline of this latest threat of account closure – looming this coming Friday – in order to allow us to make arrangements to reroute business income streams and routine expenditures, including future residual tax payments to IRD. And to allow us time to work out whether Kiwibank’s actions and conduct against us from within the banking system itself will have ‘poisoned the well’ sufficiently to prevent us getting access to the rest of the NZ banking industry at all.

So far, Kiwibank haven’t replied.

Based on past experiences, we may hear from them, or we may not. The accounts may be closed, or they may not.

It didn’t have to come to this. We directly offered the bank to engage in mediation with us several times – as has the Ombudsman – they have stonewalled this and refused. We warned them directly that if they continued to stonewall resolution, that we would pursue “all available means and all available channels” to achieve redress. As is our democratic right.

What they won’t hear in private, by necessity they will end up hearing in public.

On this blog – in the media – and if necessary, on the streets.

On behalf of everyone else in Aotearoa who may have had or be having

the same experience: this isn’t a breakup we are prepared to take lying down.

Yup, I’m doing this for you Ruth. Whoever you are.

__________________________________________________________

A note from the author: It was partly watching Judith Collins use a press conference about the silly ship that ran aground in the Pacific to lambast an Australian truck driver for having sent a mean tweet about it that pushed me over the edge on this one. There was the Minister in charge of our intelligence services gloating on camera about having used her influence, privilege and access to ID some random dude on the internet who had expressed an unfavourable opinion about Ministry of Defence personnel. It is exactly this type of wanton abuse of unbalanced and undemocratic power that culminated in the original Dirty Politics scandal in2014. Having emerged from that damaged but unscathed enough to return to Government nearly a decade later, one might imagine that she would think twice before going for Round Two. But I guess some people just can’t help themselves. The state simply cannot keep its hands out of the cookie jar. I’m fully aware – having been subjected to vast amounts of manufactured smears and state spying in the past decade – of how even daring to mention the name of the Wicked Witch of the West could backfire on me, or create further pretext to violate and abuse my rights. If it were not for Collins and her ilk, then instead of a Kiwi in Moscow I would still be, quite happily, a single Mum in Birkdale. But if there’s one thing I’ve learned, time and again – it’s that every malicious and malevolent act they commit, creates a karmic response. A WikiLeaks; a GCSB movement; a Moment of Truth; a State Services Commission Report; or…

Stay tuned.

Suzie Dawson is a former activist, journalist and political influencer now Founder and Chief Product Officer of privacy-respecting software development house Talk Liberation Limited “

Media enquires: media@talkliberation.com

I don’t think of myself as naive really, but I cannot understand why this is not in the mainstream (I don’t mean stuff) media.

We have people: Guyon Espiner, Nicky Hager, John Campbell, Matt Nippert, Rebecca Macfie, Mike White, who should be delving into this. These are the people who would not take no for an answer frankly.

When the world requires you to be a cashless society, the banks take control out of your hands.

I yearn for the days my wages would come in a small brown envelope and I had total control to determine whether I banked some or chose not too.

More companies need to follow the lead of Suzie Dawson!

Rather than rolling over & allowing underhanded business tactics that politically target (most likely in violation of anti-trust law), Suzie is taking a stand not only for herself, but for employees worldwide!

You couldn’t make this stuff up.

I’m always ready to point the well-worn finger of incompetence at the New Zealand Financial Services Industry but I don’t think it fits the bill this time.

SUSHlabs advertises Kiwibank and Westpac as clients, says they did Kiwibank’s mobile app and offers “ML & AL”, “Digital Identity Modernisation” and “AI Agent Development” services (https://www.sushlabs.com/). So what is “Dan” really? Customers are feeding it with all their sensitive, “personally identifiable information” (PII) when the latest is that “smart” phones aren’t and LLMs (a.k.a. “chatbots”) are easily hackable, e.g., https://arstechnica.com/security/2024/10/ai-chatbots-can-read-and-write-invisible-text-creating-an-ideal-covert-channel/ and https://www.404media.co/hackers-break-into-hiring-ai-chat-bot-chattr/ . Great job, bankers ! I’m strolling over to https://gogetfunding.com/panquake/ to help folks that make software and systems that aren’t about “Collecting it all” and “Selling it all” in order to make a buck at the expense of everyone else’s human rights and civil liberties.

I’m as mad as hell, and I’m not going to take this anymore! Speech from Network (1976) at https://www.youtube.com/watch?v=ZwMVMbmQBug

Suzie needs a medal for her relentless dedication to expose the powers that be, vis a vis those without a voice that are ground up by the machine!

What! No truth in advertising?

Every Revolution Needs A Leader

https://youtu.be/v-dDkbTlfEA

We Like To Keep Our Feet On The Ground Where The People Are – We Like To See Our Customers Right

https://youtu.be/2RI2IFkBO_M

No Matter Where The Decision Was Made ….. Bring An Independent Spirit

https://youtu.be/zlpERn2_ME0

True Independance – Kiwis Maverick Streak

https://youtu.be/-8fbU78r2oc

The More Independent We’ll All Be…

https://youtu.be/TvwWbwCj6s0

The Resistance- Freedom For All – Join The Movement

https://youtu.be/o75vIqTBmOw

Horrifying stuff. Let’s remember, none of this AML stuff exists for what the (foreign) governments that imposed it claim it’s for. Cops _love_ it when drug gangs and the like can use banks. It makes it easier to arrest and charge them with conspiracy charges.

No, this has always been a way imposed by the American empire and their puppeteers to crack down on political dissent, against anything that stands up against their control- as is seen in the US where it is used equally against black revolutionaries and white nationalists, and particularly against supporters of Palestinian liberation- against anyone, no matter what you might think about their beliefs and morality, who threatens to pull aside the curtain. The same infrastructure is used to block donations to organizations that support victims of ‘israeli’ terrorism in Palestine, Lebanon, and Syria.

That’s a better introduction to the saga than yesterday’s report.

Comprehensively informative.

A case worthy of every NZer’s attention.

This really highlights a bigger issue in banking, where long-term customers can feel like they’re just another number when things aren’t working in the bank’s favor anymore. It’s not just about the money – trust and relationships matter too.

Who could have forseen that it would become impossible to buy and sell?

As you identify the risk is that the criteria to have a bank account can change at any time so any dissent with those in power could result in the same fate. Hopefully you can get a fair resolution to enable you to continue the good work you are doing.