Time to cut through the weirdness, be bold and simplify Working for Families.

There is an old saying in policy wonk land that ‘you don’t make housing policy for those who live in caravans’. In other words you get policy right for the 99% majorty and if there are anomalies at the edges then deal with them separately. Crtically, don’t let progressive policy be sacrificed to protect the 1% who might be negatively affected.

I have written elsewhere about the confused purposes and principles of Working for Families (WFF). Putting the incentivising of paid work of the parents rather than the needs of their children at the heart of WFF has led to contradictory policies and an entrenchment of the worst child poverty.

But today I write about a tiny and anomalous part of WFF, the Minimum Family Tax Credit (MFTC),which, like the In Work Tax Credit (IWTC) is supposed to incentivise parents into paid work. The IWTC is bad enough, but the MFTC is far worse. For the last 7 years, it has become the tail wagging the dog, and one of the critical barriers obstructing sensible reform of incomes policies for families.

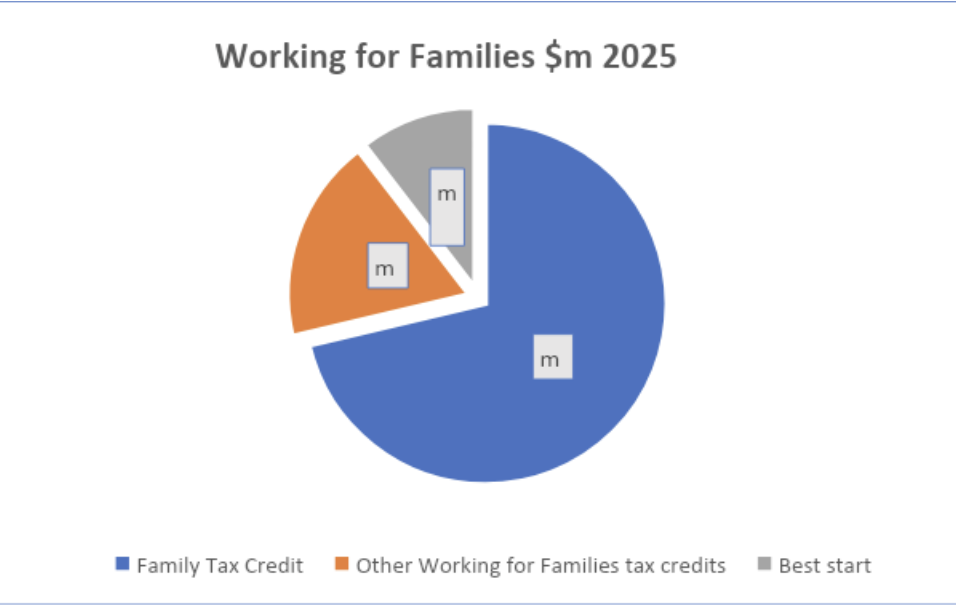

First let’s get WFF into persepctive. Of the total 2024/25 cost of WFF, $3.2 billion, over 70% is the FamilyTax Credit, a weekly per child payment that applies to all low income children. This is the tool that is best suited to tackling child poverty and shown in blue segment of PIE chart.

While vanishingly small in importance, the MFTC has been the focus of a huge amount of attention in the past 7 years with some of the most impenetrable analyses I have ever had the misfortune to read. When the MFTC was debated in parliament in 2023, the Hansard record was simply unintelligible.

A MFTC review obtained under OIA in 2023 notes

So one half of the MFTC recipients find themselves owing money at the end of the year!

In a previous 2021 blog, Working-for-families-isn’t-working-for-poor-families, I wrote

Oh, and let’s not forget the pathetic attempt to make work pay with Minimum Family Tax Credit (MFTC). A family has to be both off the benefit and meeting fixed hours of work to have their incomes topped by the IRD with this oxymoron of a work incentive. The MFTC can be a very significant state payment worth more than a part welfare benefit, however as it is paid by the IRD is not called a benefit, therefore the family can have the IWTC too. As if it couldn’t get more bizarrely convoluted, this ‘work incentive’ MFTC has a 101.3% abatement- so the family makes itself worse off by working more.

And in another, – Does the tail wage the dog I referred to the 2021 review of MFTC

Working for Families (WFF) is a $3 billion dollar programme of child-related payments, so complex few understand them. The 38 page treasury report, released this week and disarmingly titled ,”Increasing main benefit abatement thresholds on 1 April 2021 and consequential adjustments to the Minimum Family Tax Credit” is revealing. It shows little evidence that the real failures of WFF are understood. This does not bode well for the direction of this review.

This indigestible technospeak in the report focuses on a tiny, anomalous part of WFF. Has anyone actually heard of the Minimum Family Tax Credit (MFTC)? CPAG has long stopped writing about the MFTC as it is so minor, its design so poor and the number of families affected so small. The MFTC is worth less than 0.5% of the total WFF spend.

I am so tired of it as you will be too if you have read this far. BUT not withstanding all the criticisms, along with the In Work Tax Credit, the Minimum Family Tax Credit is to be increased from the 31st July 2024. The government blurb says.

The MFTC tops up the after-tax income of around 3,000 eligible low-income working families to a guaranteed minimum amount. This guaranteed minimum will be increased slightly to allow MFTC recipients to benefit from the PIT [Personal Income Tax changes] (on top of the full $50 per fortnight IWTC increase).

Remember around only 3000 families are eligible for the MFTC, compared to the 350,000 families who get one or more of the main WFF tax credits (FTC, IWTC and Best Start)

The fate of this tiny minority has paralysed the capacity to reform Working for Families Despite being something that affects so few families,and usually for a short time, the (MFTC) has been a major reason for the lack of progress on the reform of WFF.

If you want a simple story of what the MFTC is and how it works then word of warning don’t ask your friendly AI copilot.

AI’s first reply to my question annoyed me to the extent I found myself I shouting back in rage. That elicted this response: “I apologize for the confusion in my previous responses. Thank you for your patience.” But the second AI response was equally woeful. I found myself typing angrily “where did you get the information that the MFTC varies with number of children? It doesn’t— nor is that the correct formula for how it abates!!!

Copilot: “I apologize for the inaccuracies in my previous responses. Thank you for pointing that out. Let’s correct it: The Minimum Family Tax Credit (MFTC) in New Zealand does not vary based on the number of dependent children. I appreciate your patience, and I apologize for any confusion.”

After the third attempt copilot manages to get 4 out of 5 points correct. Can you spot the one that is not just wrong, but is totally and bizarrely wrong?

Copilot “Here’s the accurate information:

- Eligibility:

- To qualify for MFTC, you must meet specific criteria:

- Be a New Zealand resident or citizen.

- Have dependent children under the age of 18.

- Have a family income below a specified threshold.

- To qualify for MFTC, you must meet specific criteria:

- Income Threshold:

- The yearly after-tax income required to qualify for MFTC is currently $35,316 (equivalent to $679 per week).

- Payment Calculation:

- If your family income is below the threshold, you’ll receive the full MFTC payment.

- If your family income is above the threshold, the payment gradually reduces based on the following formula:

Reduced Payment=Full Payment−(Family Income−Threshold)×0.25

- Here, the “Full Payment” refers to the maximum MFTC amount you would receive if your income were below the threshold.

- The reduction rate is 25% of the excess income above the threshold.

- Application:

- You can apply for MFTC through Inland Revenue (IRD) or their online services.

- Payment Frequency:

- MFTC is typically paid weekly.

Good spotting, yes No 3 is the offender. There is no basis for this description of the payment calculations. I have not been able to find where the copilot got the idea of gradual reduction above the threshold. But if AI copilot doesn’t understand the way the MFTC works how can ordinary human beings be expected to?

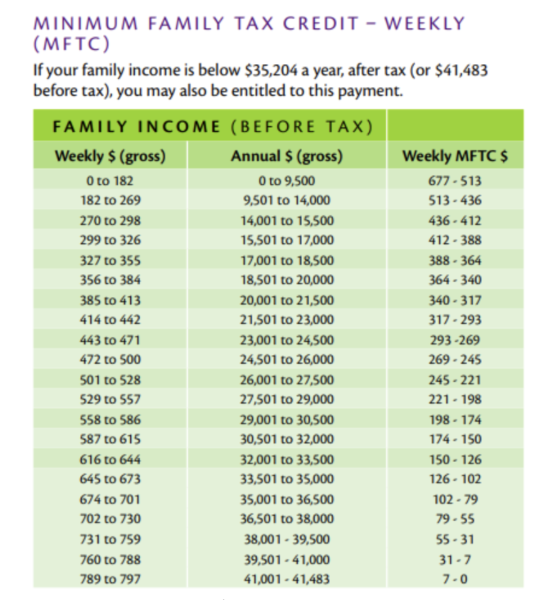

The table is from the IRD website.

The thing is that the MFTC is not a fixed amount for all families but is a top up to ensure that incomes do not fall below the MFTC threshold of $677 a week after tax, (or $798 gross income).

A family income is guaranteed to be no less than $41,483 gross.

However, even the IR table is misleading as it implies that if your income was zero you would get the full MFTC of $41,483.

But you can’t get any MFTC top up unless you are working at least 20 hours as a sole parent or 30 hours for a couple.

You might look at the table and think if you are self-employed working these hours but making very little or no income you could qualify for the whole $677 net? Dream on. The IR says very firmly on the website

The minimum number of hours cannot come from self-employed work. A self-employed person must still work the minimum number of hours in salary or wage work to qualify for the minimum family tax credit.

It is almost only sole parents who are on the MFTC as couples have to work 30 hours and few would benefit. If the sole parent works 20 hours at the minimum gross wage of $23.15 per hour she earns $463 gross. So her MFTC top up is $335 gross.

Her final gross income of $41,483 is made up of earnings $24,076 + MFTC $17407 . So far so good.

Now suppose she pulls out all the stops and works another 15 hours per week earning an extra $335 per week or another $17,407 gross per annum

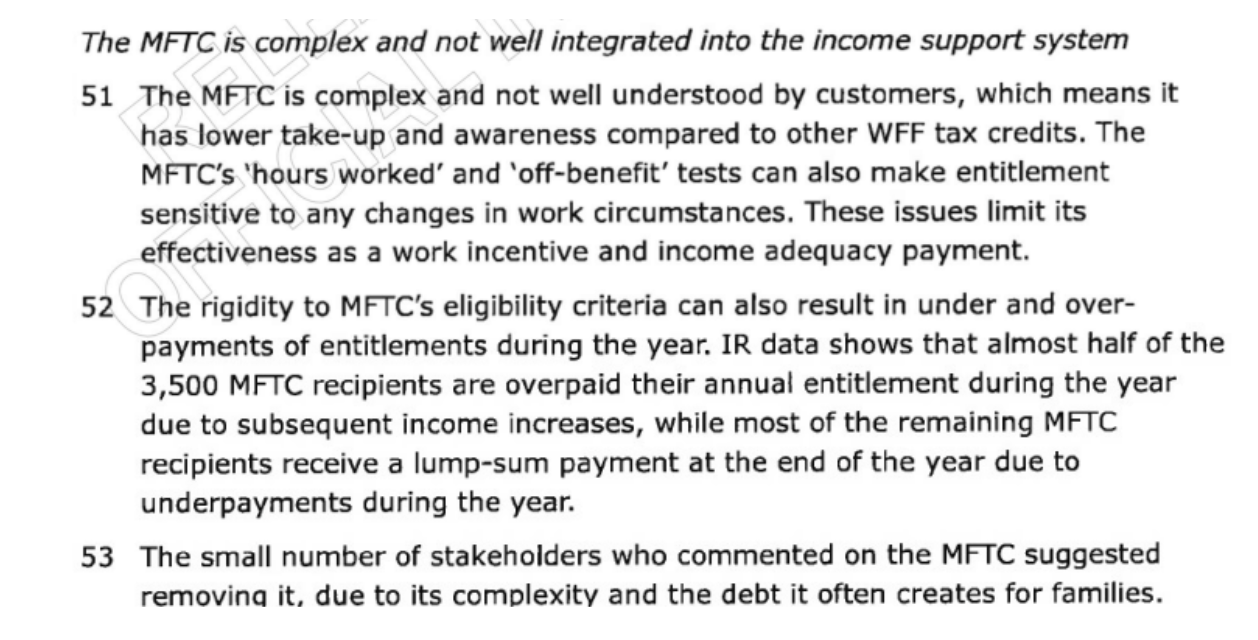

Her final gross income remains at $41,483 made up of earnings $41483 alone as the MFTC falls to $0.

What a misnomer—the MFTC does not operate to guarantee a minimum so much as act to ensure that she cannot have any more than this minimum. It sets a limit on her income and operates to provide a ceiling not a floor of income- all in the name of incentivising paid work!

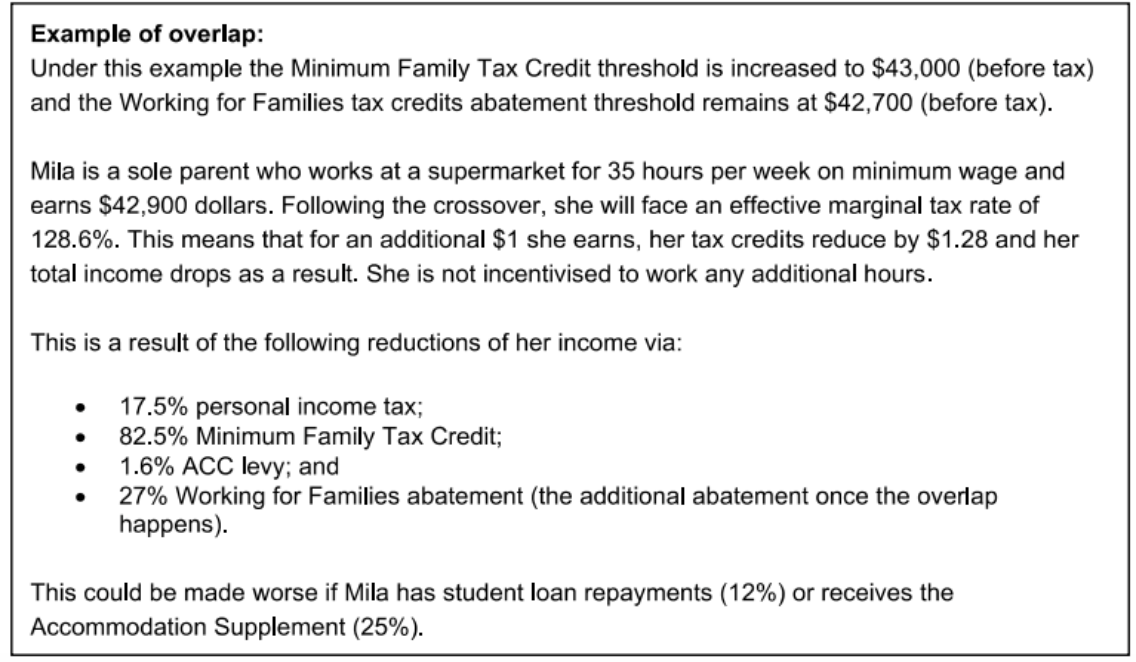

The Regulatory Impact statement, Budget 2024 outlines a bizarre scenario, whereby she faces not just a 100% abatement but a 128% abatement—i.e. works to make herself actually worse off.

At the MFTC guaranteed income of $41,483, she is just below the $42,700 threshold for the abatement of her Working for Families. For a number of complex reasons, the MFTC threshold is increased each year and the IR could see that the time was coming when the MFTC threshold would be above the $42,700 threshold for WFF.

This is a difficult example to follow but illustrates how the tail wags the dog, driving us into yet more confusion.

In the current 2024/25 year, the WFF threshold remains at $42,700. And the MFTC is $41,483 gross. If she earned $40,483, her MFTC tops up with $1000. If she contemplates earning another $1000 (43.2 hours at the minimum wage) the MFTC falls to zero and she is no better off (EMTR =100%).

So why does she in paid work at all? Under the 20 hours work requirements she has an income of income $24, 076 and a top up of MFTC of $17407 as in the example above. For the next 15 hours of work she loses dollar for dollar of the MFTC so surely she would not work those extra hours?. Thus, it is entirely hypothetical to say that if the MFTC threshold was raised above the threshold for WFF she would face an effective EMTR of 128%.

Interestingly the 128% EMTR rate was picked up in the media as scandalous without acknowledging a sole parent would have to be very ill-advised to earn to the point where it actually applied. All the while, the very high EMTRS faced by the vast bulk of low-income workers who are not on the MFTC were rendered invisible As for Mila in the example, there is often an obligation to repay student loans from $24,000 at 12%, Working for Families 27% from $42700, tax at 17.5%, the loss of Accommodation Supplement 25% and ACC 1.6%. The EMTR can be as high as 83.1% over very long income ranges.

Boiling it all down, the point of the MFTC is to ensure that a sole parent working 20 hours on a part benefit is better off coming off the part benefit and getting topped up by the MFTC and the IWTC. That way she gets more money in the hand and is considered a worthy citizen because she is not on a ‘benefit’. Ironically, she gets more state support when she goes on the MFTC and IWTC than she did when she was on the part benefit.

The fiddly process for setting the MFTC was put this way by the IRD in 2020

All of that complexity to ensure she is at least one dollar a week better off!! And can feel morally superior by being off a part benefit.

There are some important questions outstanding.

- One half of MFTC sole parents find they are overpaid at the end of the year and have a WFF debt to repay. If they incur debt by not being in paid work for at least 20 hours every week how does the IR determine that?

- If they are in debt because they earned more than IR expected- why does the IR transformation project that promised real time adjustments not sort that out?

- What happens when she cannot work 20 hours (say loses hours of work in the recession) and is denied the MFTC but cannot get straight back on a part benefit?

- What of the other income such as child support that is not taxable income but is counted against the MFTC entitlement? How does that now fit with the new way child support is now treated for beneficiaries. What other regular payments are also counted?

- And just how is ACC treated? Is the MFTC top-up the same as taxable income and subject to ACC or is just her ‘earned’ income. If it is the latter her EMTR over long income ranges is 101.6% .

Finally, why not just make it simple. Allow her to stay on a part benefit and remove the stigma. It won’t be for ever. And for goodness sake, give her the IWTC, she is earning after all. The extra $97.50 a week IWTC will usefully reduce the family’s poverty. Lets hope next time Labour gets its head around the changes it must make to Working for Families.

A little off topic, but Social Development Minister Upston, failed to keep an appointment yesterday, when she wasn’t present in the debating chamber, even though she was due to give the first speech on the the Regulatory Systems (Social Security) Amendment Bill. Consequently, the bill was discharged. This wasted the time of parliament, and probably quite a lot of taxpayers money, were someone to do the calculations of the amount of time wasted, multiplied by the number on MP’s present.

(https://www.rnz.co.nz/news/political/523000/government-bill-dumped-after-minister-fails-to-shows-up-in-parliament)

Minister Upston should show integrity and leadership and set the example for her portfolio, by insisting she receives a sanction for the breach, and have her taxpayer funded income cut by 50%, until she remedies the situation, by delivering the speech on the the Regulatory Systems (Social Security) Amendment Bill, when it is introduced later in the year. And should she commit a further breach, then the sanction can be increased to a 100% reduction in her income. Minister Upston shouldn’t receive any special treatment, but get the same treatment, she’s happy to dish out to MSD beneficiaries. There shouldn’t be one law for those at the top of the tree, and another for bottomfeeders, C listers, and tag alongs.

Since a 50% reduction in her income is still a comparatively very sizable income, that would enable someone to live quite a good lifestyle – but a 50% reduction in an MSD beneficiaries income makes them destitute in an instant. When looked at closely, any sane sensible person would say that the magnitude of a first MSD breech could be in the order of 10%, would sound far more reasonable. While the 50% magnitude that is currently applied, sounds completely wacko and out there, surely the product of some crazed out of touch MSD forensic accountants gestapo fever dream. But since that is what is currently applied, then it is only fair and reasonable and right and proper, that it should also apply to the Minister.

she should be sent to the back bench and striped of any portfolios .Where are the media on this .If she had been a minister in the last government they would be demanding a lynching before lunch .

Instead Nats and other high class strutters order a lynching before lunch.

good thoughts here. the sanctions for those on benefits for minor infringements are so diabolical. And what of the children?

This from MSD

“If you and your partner (if required) do not meet your obligations when you have dependent children without a good and sufficient reason:

for the first time, your benefit will be reduced by 50% for 4 weeks

for the second time, your benefit will continue to be paid at 50% for 13 weeks. Your benefit will restart if you undertake the activity you failed to do.

for the third time, your benefit will continue to be paid at 50% for 13 weeks. Your benefit will be increased or restarted if you agree to take part in an approved activity for least 6 weeks and you’re still entitled to your benefit.

Billy Joel has some apposite lyrics here. I feel that the likely pushers if not developers of these awful punishing systems are likely to be women. The smart no-nonsense university graduate with moral backbone! They are the epitome of womanhood and as for all the sorry sisters needing help, they are viewed in ‘ the poor are always with us’ condescension, patronised, or despised – or all together now!

https://genius.com/Billy-joel-shes-always-a-woman-lyrics

She can kill with a smile

She can wound with her eyes

And she can ruin your faith with her casual lies

And she only reveals

What she wants you to see

She hides like a child…

Cause she’s always a woman to me

Oh, she takes care of herself

She can wait if she wants

She’s ahead of her time

Oh, and she never gives out

And she never gives in

She just changes her mind

[Verse 3]

And she’ll promise you more

Than the Garden of Eden

Then she’ll carelessly cut you

And laugh while you’re bleedin’

But she’ll bring out the best

And the worst you can be

Blame it all on yourself

Cause she’s always a woman to me

Here’s an idea. How about scrapping the entire ‘Working for Families’ edifice and replacing it with a universal child benefit of $50 a week per child, along with free schooling, including free breakfast and lunch provided at school. Increase taxes above the median wage to pay for it.

Absolutely John. If we must have a corporate subsidy yours solution is a step in the right direction.

I really like the idea of free lunches but not Seymours $3 jobs. Spend $8 and get something decent.

Yes Tom cant even buy a cheese burger from Macs for $3 and its devoid of nutrition.

2 sandwiches side by side in plastic triangle in supermarket are likely to be abut $6. Quite filling – so $3 for a half which would be one whole bread slice, a half banana or half peeled mandarin or half apple and a small savoury biscuit with cheese in the mix would limit waste which would be compostable and no sugar highs and yet enough food to carry them through! But Seemore shouldn’t give his opinion on anything.

I’ll try a bit of Shakespeare adulterated, though.

Tell me where is fancy bread, Or in the heart, or in the head?

How begot, how nourished? Reply, reply.

It is engend’red in the eyes, With gazing fed, and fancy

dies In the cradle where it lies.

I think we should have family benefit this is money that women receive for their children and can make a real difference.

Has anyone analysed Seymour’s 3 lunches yet?

thats way too simple John and the government will never understand it either .

Sounds like a blissful idea, too much, John T. Parents have to be included in the system, not just in receipt of money assistance, or occasional emergency handouts. they should be looked at with respect, treated with respect, and set achievable goals for bringing up their children well. Carrots and few small sticks, Send kids to school holiday camps where they get outside and have sport and reading tutoring in short doses, and the parents who can get time off for a holiday can have their egos puffed and their experience built with workshops and group discussions with a practical child rearer. Connections can be made with parents who can later phone for short discussions about problems. (They need be short as now and then a drunken parent will carry on long-term.) The aim will not be set at ‘Zero’ anything, just improvements on set criteria improving over time.

And this is for ever, not some government magic that has reducing budgets after 3 years, and removed to set up prison coaching after 5 years. Pollies and their jesters, have a short-term memory and the stickability of tape on a wet surface.

Unfortunately John, the losers would be the low income families who are currently getting much more than $50. For example, the non beneficiary sole parent with one child gets about $240 WFF per week so you can expect income poverty to increase massively.

On the other hand, the extra unasked for, universal $50 per child for the wealthiest would make the income divide far worse and be an expensive programme that, while simple, just increases poverty

WFF is a curse!

All is does is subsidise employers and sustain a low wage economy. We need to scrap it all together.

I agree with the sentiment to ‘make it simple’. But the ‘simple’ solution described in the last para is anything but, with at least three moving parts still involved. Improvement to WFF to me are simply lipstick on a pig.

The fact that 50% of people receiving it end up in debt by the end of the tax year is a damning indictment. You get a small pay rise, you work a few extra hours and all the sudden your fixed budget is blown and you owe money to IRD.

FFS instead of trying to navigate this shit ask the question why do we even need this shit .We only arrived at this point in time because rich fucks in the 60s and 70s decided it should be the low earners that pay the most tax .That then led to more people not being able to survive because they were paying a larger portion in tax while the rich cunts were paying 20% less than the year before .

That lead to mass entry of women into the work force who were then exploited and paid low wages .Then employers could see the chance to use them to lower the wage of male workers because these poor people had two incomes now and they too might become rich .And on it went as soon governments were subsidising the rich cunts to employ the workers who could no longer cover living costs .

And here we are today with employer subsidies coming from all directions .

WFF

ACOMODATION

IN WORK TAX CREDITS

AND SO ON IT GOES .

ALL SUBSIDIES BECAUSE the rich dont want to pay fair wages or tax .

Imagine how much better it would be ,and how much cheaper for the nation and IRD if fair wages and taxes were paid .We would not need all those subsidies hence half of IRD would not be needing to take up their time on calculating how much to pay but would be able to focus on the people who are dodging tax payments and collecting the correct amount from the rich pricks who spent millions a year on tax avoidance .

Agree entirely. The left needs to unite against neolibs and stop getting distracted by tinkering at the edges which is exactly what the right want.

This level of complexity might give a duck like David Parker a stiffy and cause it to drag weed, but it is not addressing the root cause and never will.

People who work a reasonable amount must be able to support themselves and their children adequately without all of these supplements which are just the sign of a sick system they are not a cure.

Most of the tinkering at the edges in recent times has been done by Labour because they lack a spine frankly. afraid of their own shadow. It is pathetic that this party that long long ago in Adam’s time used to represent working people has gone so far down in my and many other’s estimation that the two parties have a cigarette paper between them. But the public are gullible and whilst we having all this shite done today, the public will say well Labour wouldn’t have done that and we need them back.

Te Pati Maori and the Greens are the future, will be interesting to see whether they ever vote in different directions.

No, both parties are equally responsible.

The tinkering is to win votes and power and and maintain the system.

The only difference is how many swingers will respond to a specific type of tinkering.

Yup. The Maori Party tax policy would have been a straight up tax cut for anyone who didn’t deserve to be put up against a wall.

Like many New Zealand Government systems and policies, WFF looks great from a meeting room on the 8th floor above The Terrace in Wellington, but is a shambolic nightmare to navigate.

Henry So true. It is beyond urgent to fix but both political parties want it to be about paid work. so no progress will be made and WFF debt will continue to c=climb

Reality is the whole WFF scheme is a perverse poverty trap masquerading as something good. The system leaves too many with debts to pay and the stress involved with that to the point where people are petrified to take promotion or work extra hours less they end up having to repay a large sum. I personally was burnt really badly taking a new position at work 2/3rds of the way into a financial year which pushed me over a threshold leaving me with a big repayment to make it was a complete nightmare.

The whole thing needs throwing in the garbage, I would favor a universal payment per child and additional tax codes which set a tax free threshold for parents depending on the number of children you have.

Cricklewood I can empathise with your situation here. The debt to IE because of WFF is $280m and rising. The letter that tells you you are overpaid and must repay $x,000 are quite rude and intimidating. There may be mistakes in how they got the debt figure but who has the time and expertise to challenge this.