How to stop ‘the normal principles of taxation’ destroying our economy and begin changes to create a citizen economy (Part A)

EDITOR’S NOTE: Taxation is the mechanism for redistribution of wealth to combat inequality and for redirecting resources to build a society. But our current tax principles though largely hidden or not understood by ordinary people, lie at the root of all our current inequality and struggling economy. Struggling at least for ordinary people. This article shows our current tax principles are central to our economic problems. Understand and fix tax and we are on a path to greater economic security and wealth for all, a ‘citizens economy’.

Special Analysis by Stephen Minto.

In my article ‘Housing – We can’t build our way out of this housing affordability crisis.’ on 23 August 2021 I looked at the economic structure driving housing affordability and how to solve it. I identified ‘the normal principles of taxation’ as a major factor driving excessive investor demand.

Those normal principles are helping create three of the main problems we are facing in our society:

- tax avoidance,

- inequality, generating poverty (including the housing affordability crisis),

- environmental damage, and the resulting multiple related crisis’s. (e.g climate).

These three problems show the current ‘normal principles of taxation’ are sending the wrong economic signals to the economy and distorting it away from its primary purpose, the supply of goods and services to meet our society’s wants and needs. But there is a simple reset of the principles that removes the structural drivers currently creating these problems. And a reset is essential to fix these problems as new taxes or laws will just be lipstick on a pig if we don’t fix the underlying structural drivers.

This relatively easy reset does not require any international agreement or loss of autonomy for New Zealand.

NOTE: For your convenience, we have structured this long-form report into five sections:

- In Part A we look at six ways the existing normal principles of taxation are damaging the long term economy and subsequently our society. They show the basic principles of economics are being undermined by the normal principles of taxation. I then identify the two main actions of a reset that will fix this damage.

- Part B in this series details the full range of required tax reset ideas (e.g. get rid of damaging GST) and goes through the impacts from the full reset and how many of those challenges actually put the economy on a more sustainable and stronger growth base, with more competition.

- Part C in this series covers aspects of the Pandora Papers and how it is the ownership structures of companies and trusts that are creating moral and economic problems just like the normal principles of taxation do. I raise some basic questions about how we should/could change the powers of, or scope, in which these entities are formed and operated. It is only in the structural permission about how they work that we can stop the economic problems we currently have.

- Part D in this series examines beneficial impacts and reasons why the capital revenue distinction must go. Including how it will operate and impact business.

- Part E in this series details impacts on various sectors of the New Zealand economy.

- PDF – Or you can download and print the pdf of this long-form report.

What are ‘the normal principles of taxation’?

At a very high level, income is identified by having three features:

- It comes in

- It is periodic (not one-offs)

- It has the character of income in the hand of the person who receives it.

From these base features principles arose. They have been adapted and interpreted through case law of a capital/revenue distinction. That can be defined as:

- Capital is not taxed but revenue is, so some businesses try to label items as capital to reduce their tax bill. A lot of the Pandora Papers covers this type of ‘legal’ activity.

- A sale of a farm, as a one off, is generally capital and not subject to tax. You would expect that to be reinvested somewhere rather than used to live off. But the sale of produce from the farm (periodic – used to live off) is taxable.

- Expenditure incurred to gain that ‘income’ should be deducted before tax is paid. Money spent to gain income is not really income that can be taxed.

- So you get gross income and net income.

- Expenditure incurred can’t be questioned.

- Costs to run a business can’t be questioned for taxation because it is up to the owners how to run the business regardless of the consequences or how sensible they are.

These are enough principles for my purposes; but inherent and inseparable in these principles are some values:

- tax is a cost, and

- it is legitimate and necessary for efficiency to minimise that cost. Like you would with any other cost.

But there is the catch in this, tax is not a normal cost.

Why are these ‘normal principles of taxation’ a problem?

Here are six points that explain why the principles send the wrong economic signals to the whole economy and undermine economic growth.

1. They undermine comparative advantage and encourage monopoly

(Small businesses with lower costs should have an advantage in price over big firms. But larger firms use costs to reduce their tax to give them an advantage.)

- Business is supposed to be efficient and reduce costs, to be competitive. The theory goes, by driving down costs you drive down price which is better for satisfying consumers wants and needs. This is more efficient and only business can do this as government is wasteful and costly.

- But this same efficiency driver on a micro business level sees tax as a cost that a business gets nothing for on a balance sheet. So to avoid tax, a dead cost, the ‘normal principles of taxation’ allow them to grow other costs to not only prevent having to pay tax, but also to do things that drive up the price of their goods and services so they gain more profit.

- We all know and experience the marketing techniques that large business use to keep their profits high, or how they run anti-competitive practises to undermine competitors. e.g. run an airline along the routes of a competitor so they don’t grow and move into their high cost routes. And these techniques cost a lot. They rely on big data from loyalty cards, slick advertising, changing superficial designs with new releases, glamorous shops, etc. And they rely on access to debit financing. These are just ‘normal’ large business practises based on behavioural/marketing psychology and finance.

- So large businesses don’t mind incurring these costs because they will reduce the ‘dead cost’ taxation they have to pay. And it is a big saving, 28% on every dollar spent. So consumers/taxpayers in having a reduced tax are actually helping large companies pay for techniques to make us pay more money for their goods or services. So we pay twice for their supplied good or service – once on the high/‘discounted’ price and second through the tax subsidy.

- Small businesses simply can’t afford to run the same techniques or access debt finance in the way a large firm can. Their whole pricing structure is done differently; they reduce their costs and run a tight ship. These economic rules simply don’t apply to large business because the normal principles of taxation turn costs into an asset for them – a tool to drive out smaller competitors while driving up price. Small firms can’t compete against these large firms no matter how good the quality or price they charge for their good or service.

- Another perverse result is large businesses become less concerned about quality and service in part because like any large bureaucracy they have to wear a few problems. But also in part because large businesses not only compete on price and quality, but compete through ‘cost accrual competition’. The ability to accumulate costs that work to their advantage over smaller competitors. And it is profitable and relatively easy and ‘legal’, but it shifts a large business’ focus away from innovation and building quality or low price, and into a focus on gimmicks and primal manipulations to trick us to buy. And it reduces competition as smaller firms can only compete by reducing costs and there is a limit to that.

- We can see this most easily in fast food and retail where there has been a slide into franchise. The Chemist Warehouse is one of the most recent. Costs on the floor are tight but the marketing, site location rental, management fees, executive salaries, advertising, debt financing are all high cost. In a generation the smaller owner run businesses taking pride in their business are largely gone from New Zealand. So many small businesses struggle and fail because it’s hard to find niches to escape the larger firms relying on costs and turnover to drive their pricing. Cost efficiency is no longer a key economic driver for a large business; ‘cost accrual competition’ through saving tax is the easiest way to wealth.

- In addition larger businesses are more likely to spend on vanity expenses because it still reduces their tax bill so it gives them an advantages over smaller competitors. e.g. take a lease on property in prestigious locations, purchase on finance or lease luxury cars, still get a 50% deduction for business ‘entertainment’ expenses – meals and lunches, tickets and who knows what else.

- ‘The normal principles of taxation’ remove the natural competitive advantage of a low cost business supplying the same goods and services. These smaller business are normally New Zealand owned and operated. And to catch that advantage all businesses have to follow that high cost model, and treat tax as a cost to be minimised, leading to larger and larger businesses leading to monopoly capitalism. Cost accrual competition is a powerful economic tool and we the taxpayer are subsiding it to only some people’s advantage.

2. They undermine redistribution of wealth (tax) and the resulting economic stimulus

- Almost all businesses do not create wealth, they simply accumulate wealth. And to accumulate they rely on the education and health systems to support access to employees and customers. They also rely on infrastructure, courts, police etc in which to do business. Tax minimisation, avoidance and evasion, undercuts the process of redistribution of wealth which pays for the supply of these services and therefore it undercuts the provision of the services the business needs to function with.

- Redistribution by taxation also supports demand across the economy which in turn supports business accumulation of wealth. The ‘tax is a cost to be minimised’ attitude comes from the normal principles of taxation, but tax helps promote the multiplier effect which benefits the entire economy. The principles need to change so that no business has an incentive, and mechanism provided by the principles, to minimise tax, as it works against the long term supply of goods and services, within the economy.

- Tax is like no other cost as it is not fixed. The principles calculate it as a relative cost based on what income is left over after costs. So on a micro economic level a business see’s an advantage to run up costs to minimise payment of tax. But on a macro economic level that minimisation is damaging the economy in which it functions. Tax minimisation is actually an act of self harm by a business in the long term. The normal principles of taxation are creating the problem.

3. They subsidise risk taking and provide no choice for taxpayers on doing that.

- By allowing business to deduct expenses to reduce their income that is liable for tax; it makes the New Zealand taxpayer subsidise the provision of that good or service through sacrificing tax collected. And as said before the saving is not always passed on, prices are held high and profit maximised so consumers are not getting the benefit of the subsidy. The normal principles of taxation allow no choice for society on making this subsidy. e.g. huge amounts of investment resources can be used to subsidise the business of taking rich people on tourism flights to space. Would people vote for that choice, over lifting more children out of poverty? But there is no vote, we have no choice, and it is tax revenue we could have.

- The entrepreneur who has the knowledge to make these choices about what costs to incur should take the risk for those choices. Choices and risks should not be subsidised by taxpayers or government as that is not their role.

- If the people or the elected representatives decide to subsidise an activity that is okay. And that is very different from a blanket subsidy as happens currently under ‘the normal principles of taxation’.

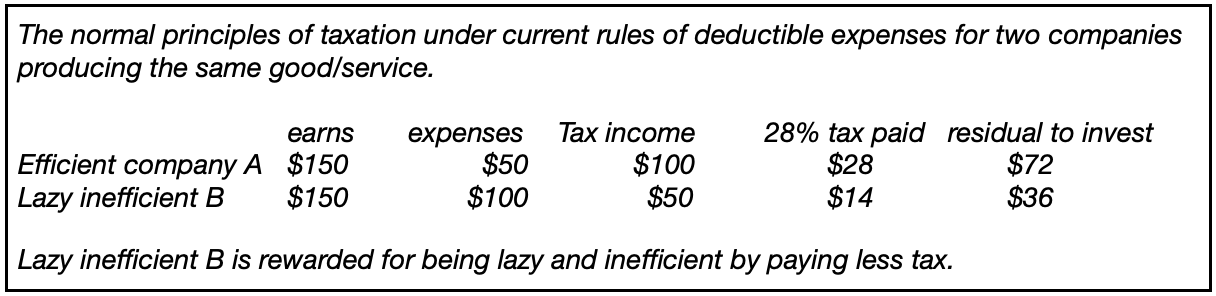

4. They punish innovation or the efficient use of resources

If two businesses supply the same good or service but one does it at a higher cost than the other, why should the lower cost company pay more tax? This is not good economic policy.

- The Lazy Inefficient company B has more expenses ($100) so only pays $14 in tax but the efficient/innovative company A ($50 in expenses) pays $14 more tax at $28.

- The normal principles of taxation are sheltering poorly performing companies, and punishing well performing companies. And the taxpayers through having less tax collected are subsidising the inefficient poorly performing company.

- And the principles allow more investment income to be made available to this poorly performing company. i.e. wasting scare investment capital. (If B did not get the tax subsidy and had to also pay $28 in tax like efficient company A, then Lazy inefficient B would only get $8 to reinvest).

- To those who say the high cost of B could be due to the quality service they provide. Yes, and that will mark them out from their competitors, and that quality should sell them. But there is no way for the blunt instrument of taxation to tell the difference of quality to wasteful spending; so it shouldn’t. If customers don’t want that business’s ‘quality’ then that is a market signal. There is no reason for the taxpayers to subsidise a business’s choices on quality as the entrepreneur might be right or wrong and there is no way to tell, except by the customer.

- More can be said on this example but it does not change the fundamental point that the wrong economic signals are being sent. e.g. Company A could have less customers and be price matching to Company B to maximise their profit rather than passing on the savings from innovation to their customers. Company B becomes a tool to make customers pay more as its existence takes up some demand, which slows the introduction of potential new competitors. This is another reason to have B out. This shows tax is only part of fixing the economy but a very very important part.

5. They subsidise environmental damage or resource waste by creating an externality

- Of course not all companies have high cost structures because they run anti-competitive practise, or have vanity expenses, or they are just seeking tax minimisation. Some businesses, are just very costly to undertake and there is nothing inefficient about that, e.g. mining.

- But should the costs to run those enterprises be subsidised by the taxpayers taking a reduced tax collection? The high costs of those business choices should be borne by the risk taking entrepreneur with the knowledge to take those risks.

- For example, if you do the Hump Ridge track you see some great wooden viaducts used to bring out the timber from a milling operation. The devastation of the local forest was complete but the business as reported never made a profit as its costs were so high and the sales income never fully came in. New Zealand got nothing of substance out of this destructive exploitation. Yes workers got wages and scrimped a life of remote hardship. The directors would have got income along the way. Yes there is now some tourism value but it’s probably not much more than if it was left. Overall, the value of the forest asset was wasted without profit. The ecological and cultural value lost can’t be quantified.

- The same destruction and waste occurred in the areas around the ‘Bridge to Nowhere’ in the inner Whanganui. All over New Zealand subsistence businesses were supported by ‘the normal principles of taxation’ for people to eke out an existence to the detriment of traditional Maori life and culture, the environment, and their own lives. The ‘normal principles of taxation’ were one of the systems within colonial exploitation that allowed profits to be stripped back overseas without as much redistributive effect from an effective taxation. The principles were a tool to strip value out of the new nation as the costs of exploitation were offset to the income. It is a tool in a class system that strips income away from the redistribution/taxation process.

Colonial legacy justification and creation of an externality

- Yes, you can argue that this sort of tax subsidy for business was necessary to enable economic activity in new lands. And that is the colonial argument. From where we stand today we can see the waste and destruction of that legacy and thinking. Our climate and environment is imperilled because of it. But it’s still happening, that structure is still in existence within the normal principles of taxation, and it is helping drive environmental damage and climate change. The rules were made through judge law to favour the wealthy to help drive their, or their class’s, wealth. This reset will at least make the full cost fall on the risk takers and they will at least be more careful in future because the cost will fall on them fully.

Ongoing impact

- If income from a business activity almost matches the cost of the activity, then very little tax is paid. So when the good is being sold the price does not reflect the cost of society’s human and physical infrastructure that was required to support that activity. Because tax was reduced this cost is not calculated into that sale price. i.e. a seller will work for the highest price but if the cost of production is subsidised, the threshold for the sale price is being subsidised and the true cost is not reflected in the price resulting in false economic signals being sent to producers. The normal principles of taxation are creating an externality of the cost of society.

- A business must fully contribute from its income back to society through paying tax or there is no point in society letting the business be in existence. Like the purchase of the viaducts, or the mill boilers, tax is just a cost that should be factored in and you can’t avoid it.

- Each business or activity needs to be viable in its own right so it has a cost that reflects if it is a high cost activity. Current loss offsetting hides a costly activity and dissuades companies funding research or looking for alternatives to get around high costs. Subsidising by tax undermines that drive for innovation.

- Environmentally damaging activities like mining are one such activity where if the cost of tax was not able to be avoided, a higher price would generate more focus on recycling, or innovation to find alternatives. See more comment under heading ‘Different sectors have different impacts’

- It is no longer appropriate for our business community to be molly coddled and subsidised by socialising their costs onto the New Zealand taxpayer, the government, and the environment.

6. The ‘normal principles of taxation’ are helping cause an international destabilisation problem.

- President Xi in China is crushing democracy in Hong Kong as he see’s it as a vehicle to undermine China. But he is fighting the wrong enemy. As a former colony of Great Britain Hong Kong follows the basic outline of ‘the normal principles of taxation’. And most of the tax principles were set through english case law by judges who arguably have acted in their own or their class’s economic interest when making decisions that set precedent. As a colony these tax principles facilitated economic value being stripped away from the colony and the lands near it to the benefit of the ‘mother country’. In the post colonial world we still see these tax principles being used to strip value out of countries with little tax paid, and then into tax havens for the use of the billionaire owners of Google, Amazon, Microsoft and others.

- China has become the factory of the world as large multinational companies moved manufacturing there for cheap resources and low regulation. President Xi wants the work and business to stay so it will give stability and economic strength to China. He was recently reported on CNN Aug 18, 2021 by Laura He as pushing on China’s rich to redistribute wealth. So he can see problems in his nation but he is asking business people bound by a tax system to act outside that system. His quest for security by taking on democracy and the Uyghur people means he is no longer walking with his people as a leader, using the wisdom of the crowd to guide his nation but is leaning into an inherently unstable autocratic leadership model. And he is adding fuel to the cold war that leaders in the US, UK and Australia, seem willing to hype up in a new alliance. He has chosen the wrong enemy; it is the colonial based tax structure that is undermining China’s security, e.g Transfer Pricing and Thin Capitalisation are able to undermine revenue and the ability to grow domestic based businesses in a way that spreads wealth. That has to be dealt with by simple consistent rules as suggested here that do not favour multinationals, as the current normal principles of taxation do. Democracy needs to be decoupled from exploitive capitalism and a tax reset will help do that.

- And the ‘west’ is also struggling with conflict and polarisation in society, driven through culture war issues like immigration, climate change, vaccines, and abortion rights. In the ‘west’ the culture wars are facilitated through a dysfunctional 4th estate and poor quality democratic processes. These culture wars have some urgency for ordinary people, ‘taking our jobs, taking our opportunities’, but theses are just the scapegoats for the very real economic struggle many are experiencing. It’s about the economy getting polarised. Ultimately the western nations have the same enemy as China in the poor functioning of the tax system. The tax system is helping build monopolies, facilitating tax avoidance, and undermining local businesses. We are all poorer.

- The normal principles of taxation are well overdue for a complete overhaul so they build each nation’s economy and redistribute wealth, and that is the purpose of taxation, not to concentrate wealth and build tax havens.

- Note: The need for international trade by New Zealand will not be impacted by these changes but it may, or may not, modify it. And with the supply chain disruption brought by the Covid-19 Pandemic, it makes it an excellent time to bring in changes that will ameliorate the disruption we are already experiencing. It will help our nations build back on to a more sustainable path.

How shall we reset ‘the normal principles of taxation’?

- In the media and policy world the strongest reset theme for taxation is greater transparency and sharing of information from other jurisdictions (especially tax havens) so tax can be claimed. This is all essential work that needs to be done but transparency and sharing information does not remove the structural problems created by the principles. And the current principles have created a complex set of rules that are an administrative burden.

- And the creation of new taxes like wealth taxes will not deal with the structural drivers of wealth concentration. As the Pandora papers show the normal principles of taxation are a major driver of wealth concentration and tax avoidance.

- I propose a structural reset that uses existing economic understandings which therefore won’t destabilise the economy, and it works alongside the existing market forces, sending appropriate signals to the economy.

The two main reset actions are:

- Remove deductibility for all expenses except for domestic salary and wage payments.

2. No capital revenue distinction for non-individuals.

This is supported by:

- A very broad legislative definition of ‘income’ to ensure everything that comes in is taxed regardless of traditional capital revenue distinctions. Even to include related party loans (with an exception for 3rd party loans – perhaps a strict list of who can be a 3rd party). The Pandora papers show this is essential regardless of even this reset. Because the current normal principles of taxation allow a company to make income but then through a series of entities turn it into a loan to be made back to the company or another related party and a ‘loan’ is not taxable. Part C, in this series, gives an example.

- No grouping of companies for tax purposes. Companies are separate legal entities and will be treated that way for tax.

- The original intention of grouping was to prevent tax avoidance but it has now been twisted to be a major tax minimisation technique. i.e. Company tax rates in the past had a progressive structure. To avoid paying the higher rates a company created lots of sub companies and spread the income out so each paid an amount just below the high tax rate. This was then stopped by the requirement to group the companies so they did pay the higher rates of tax. But then for anti-competitive purposes parent companies began to run subsidiary companies – not to make a profit but to make a loss (the exact opposite of what companies should be set up for in an economy). Using ‘cost accrual techniques’ and low income. e.g. run a small airline at a loss to compete with a budget airline to preserve their other profitable routes. Grouping then allowed their losses to be offset against the income of their profitable routes so less tax was paid. If a situation arose where the loss company was no longer needed the losses could be retained but limited liability remained as a protection for the parent company. A long time ago the progressive tax rates on companies were removed and company tax was made a flat tax rate but nobody got rid of this ability to group companies. The companies wanted it kept. It is overdue to get rid of grouping.

- Without a capital revenue distinction and strict application of entity status, shifting assets between separate legal entities will generate taxable income because their status as a separate legal entity now becomes important for tax purposes. With less advantage in having separate legal entities, companies will become bigger which will improve transparency and reduce the ability to avoid tax or scrutiny. This reset will work with international trends to improve transparency. With more potential exposure to risk, behaviour and focus will change.

- A company to trade in New Zealand must be required to have a company registered and based in New Zealand through which all its activities are subject to tax that are ‘sourced’ from New Zealand. And they must have a New Zealand bank account. An asset in New Zealand can’t be owned by a foreign based organisation in a tax haven as the risk of tax avoidance is too high. If there is not a base in New Zealand, e.g internet sales, then work must be done with banks on how sales can be caught for tax or punishments if not. This is already a tax issue and not created by this reset.

- In ‘Part D (of this series) – Beneficial impacts for all with no capital/revenue distinction and less tax minimisation’ I go through more discussion of these points. In particular how taxing disposals of cash accumulations is not double tax but sends a beneficial push into quality and price for goods and services.

Economic policy and tax principles alignment

This reset does four main actions:

1. It removes the structural drivers for all the six economic problems listed above. Obviously other actions need to be taken in addition to tax for issues like international relations. This reset does not restrict actions but better supports them.

2. It stops almost all tax avoidance techniques based on currently ‘legal’ processes. Nobody is telling business how to run their business or control what they do. The choices are all still with the business, it is just the consequences and risks that will be fully carried by the chooser.

3. It removes any incentive to waste or damage the environment, or any assets, as all costs will be fully carried by the producer. Because things will cost more, the throw away culture will not be structurally supported by the tax system. Note – things are costing more now but with no quality improvement. Quality has the chance to come back.

4. It redirects investment capital to producing goods and services to meet the needs of society. With interest no longer deductible for tax there will less demand to debt finance. Finance will therefore be freed up for investment in actually producing goods and services. Yes some capital will be taken up to hold assets like land but that is a good investment at the moment. The purpose of debt financing is largely cost accrual competition. Part B of this series has more on the potential positive changes in how investment may occur.

But is this economically viable? We must look at the numbers.

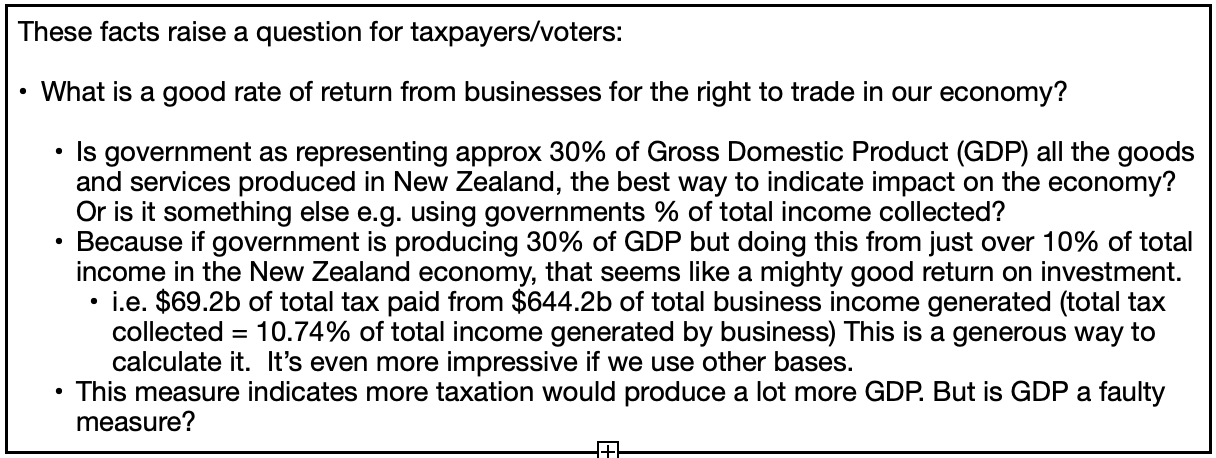

Financial impact of reset

From the Statistics New Zealand website we have the ‘Annual enterprise survey: 2017 financial year (provisional)’.

It states for businesses/enterprises the:

- total income for New Zealand is $644.2b (billion) and total expenditure is $560.7b.

- Surplus potentially subject to tax = $83.5b (If the current tax of 28% was applied, this = $23.38b)

- 2017 Inland Revenue Annual report, says corporates actually paid $14.2b.

For contrast from the Inland Revenue website 2017 annual report –

- Total tax in 2017 was $69.2b and Individuals paid 48% ($33.2b) plus GST 26% ($17.9b) = 74% of total tax was paid by you and me.

Taxation under a reset calculation – A soft transition calculation

The existing tax rate of 28% could be used or a lower rate of 15%. But if we aim to increase taxation because it is sorely needed for social purposes, and to pay down debt, and we don’t want to cause too much business disruption, then the following is an option.

- Businesses claimed they had $83.5b income over expenses for the 2017 year.

- If we initially taxed all companies at 10% of total income, no deductions for costs (except domestic salary and wages). And indexed to go up in future years. This will give a massive boost to small business.

-

- $644.2b x 10% = $64.42b tax.

- As business had $83.5b over costs it means there is income available to pay the $64.42b tax. They would have to shift profit expectations and likely no dividends. Impacts will depend on the individual business. If we add in the Individuals tax, and ‘other’ ($37.1b) tax paid that year (I leave out GST as it must be dropped – as it damages the economy) we would have: a total tax for 2017 of $101.2b

- The amount of 10% should be indexed to go up 1% every one, or two or so years, until it reaches 15% or 20% or whatever the government of the time decides. The 10% rate is too low for the urgent needs of climate change and human need. (The cost is higher now because actions were not taken earlier, and business in aggregate has not supported taking action sooner, in fact they hindered action).

Other taxes?

- This increase in tax collected is without any new wealth tax or capital gains tax, and with a reduction of the headline tax rate. But there may be other reasons to do new taxes. In times of war. Or environmental crisis. Or a housing crisis. Tax is so low at the moment and the social needs so pressing, plus the debt must be paid down, that the amount of tax to be paid must go up.

Easier compliance

- Another reset benefit is it could be possible/investigated to require all money deposits to a non-individual to go through one bank account with an instant deduction for 10% tax. A credit can come back once a salary or wage payment is made in the Inland Revenue employer account. This means no provisional tax or due dates to worry about. A great compliance saver for small business. Obviously all bank accounts would have to be linked to an IR number to prevent avoidance but if all non-individuals bank accounts were automatically subject to tax, then that removes some temptation to avoid tax liability.

The economy context

- This reset is still only income that is being taxed; something that has ‘come in’. So money is there. Any realised capital gains would also be taxed because they would have ‘come in’. But as there are avoidance techniques for companies to delay gains coming in I am not expecting much to be collected under this category, initially. But a rising tax rate might persuade them to come forward earlier. But we could use the ‘risk free rate of return method’ to calculate this ‘income’. But that would be at least 15%. Other options to capture unrealised gains are being discussed in the wider media.

- If large businesses say they will go out of business, then that shows just how dependent they are on the tax subsidy. So are they truly viable? The slow introduction of a lower but more effective rate would give them time to adapt to moving away from debt financing, and high cost structures. But there are many more effective ways to achieve this change. I don’t expect them to move away from their marketing techniques but they would pay that cost without being subsidised by taxpayers. Issues with marketing and consumer protection can be dealt with separately but those actions will be undermined by the current tax system. Actions will be more effective with a tax reset.

- To stick to the concept of government spending being less than 30% of GDP reduces our ability to create wealth through the multiplier effect. A demand driven economy will bring better economic growth that actually satisfies people’s needs. The only risk to a demand driven economy is how to control pricing and inflation, (I propose an article on this at a later time). We tried supply side economics and we have poverty, housing shortages, housing inflation, a struggling health sector, and an education system beholden to overseas students.

Perfect timing

- The recent talk about inflation and stagflation in part due to supply chain disruption make it the perfect time for the reset to happen as it will reduce business sector demand. All large businesses will be strongly focused on reducing their high cost business structure which will reduce demand and take pressure off inflation. Recall that a lot of business sector demand is micro business churn to drive price and demand up for their product or service. It is not growing the economy except in an incidental sense. Innovation, exports or savings are not being driven in the macro sense by that spending. By contrast small businesses with the lower tax rate will be opening up, increasing competition. I talk about inflation in Part B of this series but will require a further analysis.

Summary – we must reset ‘the normal principles of taxation’

- This reset is not about political sides or ideas. It is about making the economy work as it is supposed to, meeting people’s wants and needs.

- If we believe in markets with businesses competing on price and quality then this tax reset must be done because the current tax system undermines that, or

- If we see the economic system is failing and people are falling through the cracks then this tells us one of the main reasons why and how to fix it.

The current tax system is breaking the economy and society. We are a frog in a pot that’s been on the stove for a while.

- Further evidence the tax system is broken is seen in the US which has the same basic principles of our system and many of their largest companies aren’t paying much tax, e.g. Amazon, Honeywell, Halliburton, IBM, Fedex, Nike, US steel, Chevron, Delta. These companies are even managing through globalisation to avoid capital gain taxes. So we can’t just rely on new taxes to solve the existing problems. The foundation, ’Income tax’ must be fixed and this reset is how to do it so the big companies pay their fair share.

- Minimising tax is big business for every large firm. For the cost of a small team of accountants they can structure finances to avoid billions or hundreds of millions of dollars in tax. The purpose of tax is to redistribute wealth but ‘the normal principles of taxation’ are discouraging redistribution so economies and societies are struggling, with small businesses disadvantaged and people’s wants and needs not being met.

- The reset here retains largely the same tax system with all business treated the same. But the reset strips the rules down so there is nowhere to hide or shift the money. Because it is in the rules where the loopholes are found. And the rules/legislation are written with the normal principles of taxation firmly in mind, and with considerable input from those accountants who are deeply embedded in tax orthodoxy. The business sector has had a significant input into developing tax law and the business sector likes lots of red tape rules as it offers lots of loopholes.

- In this reset you can’t shift money between income (subject to tax) to capital (not subject to tax). A person can’t reduce their tax by claiming expenses real or imagined. There are no losses or capital losses. I suspect the reason why we don’t have a capital gains tax in New Zealand is the fear of capital losses undermining future government revenue along with complexity of the law – but this reset shuts down those fears.

- With this reset the tax system becomes much simpler and more transparent. This is why stripping the rules back, as is proposed in this reset, is actually the only way to get a truly broad based low rate income tax system.

Note: Even if the government only takes the tiniest initial step along this path by removing the deductibility of interest. This will slow the incentive to debt finance, which will undercut many of the negative tax practises. And with lower demand for loans it will help redirect investment to new projects or innovation. We will start the journey to a more efficient tax system that builds the entire economy and society.

It is overdue to change ‘the normal principles of taxation’. Write to your MP’s and tell them so over and over again. Because some self-interested businesses do the opposite, a lot. They forever talk about black hole expenditure and of this situation or that. Just recently the government allowed deductions for feasibility expenditure – that is normally capital expenditure and not a deduction. So the rules are going one way all the time to allow more and more costs. This reset removes most of that and simply moves the dial back the other way. This reset is not breaking the tax system anymore than it can be said the feasibility changes are. We all know from the Pandora papers the income tax system is stuffed but surprisingly it’s not impossible to fix.

———————

In Part B of the article ‘Creating the citizen economy’ I expand what is involved with a comprehensive reset and outline the key impacts.

- In Part A I outlined the problems the current principles are creating and I outlined the two main changes.

PART B – The six reset actions in New Zealand – for the normal principles of taxation

The six actions are:

1. Remove deductibility for all expenses except for domestic salary and wage payments.

2. No capital revenue distinction for non-individuals (variation for a private home in a trust or other entity).

3. Imputation and other related memorandum accounts should be ceased.

4. Introduce some restrictions on charitable status, and donations.

5. Remove GST as a tax (alternative taxes could be considered to replace if needed).

6. Tax evasion (tax avoidance is dealt with by the above proposals) become fully engaged by the New Zealand Police – financial intelligence unit.

1. Remove deductibility for all expenses except for domestic salary and wage payments.

- A deduction for domestic employment gives encouragement to employ people, and to reward them well is not a drag on the business (e.g. no claim for wages if you set up a call centre in another country). Easy to audit the claims as domestic salary and wage records are kept within the NZ tax system.

- This removes cost accrual competition and reduces the opportunity to avoid tax. It would structurally set the idea that tax is just a cost that business must pay.

- This action gives comparative advantage to low cost locally based businesses. This will encourage small start ups. Small businesses allow more opportunity for ideas and innovation to be pursued. It encourages peoples enthusiasm to pursue their ideas. More people are employed in small businesses.

- This action simply aligns costs that set up the business (capital and not deductible) with costs to run the business as (revenue and deductible) so neither expense is deductible for tax (Just like employee’s aren’t allowed any deductions). Currently larger companies find it easier to set up intervening companies which will incur the capital costs but then on-charge the capital costs through the intervening company so they look like revenue costs. This sort of tax minimisation ceases. Smaller companies benefit.

- It will promote fair competition, and economic efficiency by recognising the above comparative advantage of a business with a lower cost structure, leading to less waste of resources while encouraging New Zealand based business which could lead to a lower carbon footprint.

- The tax system would be easier and less costly to comply with and administer. It would also make the introduction of the second reset action much simpler and less complicated.

- There are several significant impacts which will change the way business is likely to be organised (see below for a discussion of impacts). Just as the existing ‘normal principles of taxation’ are encouraging negative behaviour, the reset will encourage positive behaviour.

- Drawings would have to be paid through the IR employer system to be credited for deduction so taxed when received and included in social policy calculations. Or there is no deduction and it would still be required to be declared as income.

2. No capital revenue distinction for non-individuals (variation for a private home in a trust or other entity). [This means all money coming into the business is subject to tax unless expressly exempt. Currently if something is called capital you don’t need to pay tax on it. But with the reset all disposals of an asset are income, unless expressly exempt.]

- The objective is to simplify taxation and remove the opportunity to re-characterise something that is income into something that is capital to avoid tax. Currently capital ‘income’ (a one off) or ‘gain’ is not taxable because it is not considered income. The reality is this is an accounting fiction for a non-individual. All actions by a non-individual advance the financial interest of that entity so its essence is one of generating income. Like a trader who buys and sells things that are capital items but if you sell with an intention of profit that is taxable. A non-individual often acts as part of a network of entities, or in a scheme of actions, so all actions have the character of income for a non-individual.

- Variation is just to allow a person living in a home but under a trust ownership, (somebody might need to protect the home so it is not lost in a business failure or loan situation) to continue to do so. One house only. It would probably need to be a public list to ensure compliance is not an issue. But perhaps there are other ways.

- A reset would require a legislative definition of ‘income’ for non-individuals. It would be simple like the feature ‘it must come in’. This would mean realised gains are taxed because liquidity of some sort is available to be taxed. The complexity to track gains drops away if we are just tracking the gains without considering expenses (although using the ‘Risk free rate of return’ method could be done and may be easier). Public companies must publish their financial accounts and they use this to promote their companies so I think the hiding of gains would not be easy. Some work would need to be done to ensure ‘off balance sheet’ gains are included. With a wide ‘income’ definition some specific items could be removed by an exemption (e.g. loans from 3rd parties). In Part C I give a situation where income is converted to a loan so it is not taxed. To stop this requires a very wide definition to be applied.

- There would be no losses because it is just gains – ‘it comes in’. There are no expenses to create losses. There would be no allowance of historical loses to roll forward. The risk of the loss remains with the entrepreneur, who has the knowledge to take the risk. Rather than the current situation where losses are socialised through the tax system by a reduced tax take.

- This is not a capital gains tax but a definition of ‘income’ issue. Much like the government of the time with the introduction of the ‘Bright line test’ for property ‘rightly’ saying it was not a capital gains tax. And even if some do make the argument it is a capital gains tax this would still be false for individuals, and the fact that you can turn income into loans under current rules shows it is just an income definition issue.

- There are some big challenges and changes to how business would think and act for: exports, speculative business, high turnover business, (see below for a discussion of impacts).

- Because all disposals of an entity’s assets (capital) become income this changes how some items are viewed. A cash accumulation is an asset. So to send this back to the parent company will mean it is taxed. This has a positive impact on reinvestment in the company. For example, an aged care facility makes profits from caring for elderly residents. Profits can be reinvested to improve services or bring down prices. This is the purpose of the market mechanism. But it is hard to enter the market for aged care business to create a bit of competition (if we want that), meaning the market mechanism doesn’t work that well. So taxation on disposal of profit to an entity outside the company will have the effect of encouraging funds to stay in the company to improve services and pricing, and grow the business through quality and price. In the current tax framework there is too much focus on profit extraction to the detriment of service and quality. However we can predict that the reaction will be to make companies bigger so money is just transferred between units or sites. But still for assets to leave the company it will be taxed. Companies will have to be more careful about structures to ensure they only pay tax once when it leaves the company.

- More positive impacts are given in ‘Part D – Beneficial impacts for all with no capital/revenue distinction, and less tax minimisation.’ which will build better more responsible companies with less tax minimisation.

3. Imputation and other related memorandum accounts should be ceased.

- It was said to prevent ‘double taxation’. i.e. A person with a 33% personal liability for tax gets a credit for the 28% tax already paid by the company when the company pays the person a dividend. The person then just pays 5% extra or whatever rather than 33% or 38% on the dividend. Removal of the credit would function like a sort of wealth tax so they do pay the 33%, or 38%.

- Currently imputation encourages the payment of dividends to shareholders which strips investment capital out of companies. The prospect of taxation would encourage capital to remain in the company for growth, which is good for our economy.

- Easy to administer and collect as with payment of a dividend there is clearly income available, and it can be taxed at source. As income it avoids complaints about disposal of assets to pay a tax, which a wealth tax raises. (I’m not against wealth taxes, it’s just it still leaves in place the distorting income tax foundations, ‘the normal principles of taxation’, that lead to monopoly capitalism which necessitates the wealth tax).

- The traditional avoidance mechanism of bonus share issues would need to be prevented or declared taxable for an individual (with simple rules not complex ones). For a non-individual the receipt of a bonus share would now be taxable with no distinction of capital – revenue.

- Because of imputation, tax rates on wealthy people in New Zealand are low and they are the main benefactors of dividends.

4. Introduce some restrictions on charitable status, and donations.

Amend advancement of religion exemption

- A church/religion doesn’t pay tax on a business if they are approved as advancing religion. In a tolerant society your choice of religion should be your own and that personal choice should not reduce a citizen’s wider commitment to society by paying tax.

- It is harder in the modern world to see how the advancement of religion is a positive to society, e.g attitudes to vaccines, women etc. Perhaps this exemption should only apply to that income used solely for the relief of poverty, the sick, or those in prison.

- The tax exemption means all taxpayers are in effect subsidising a person who might knock on your, or your neighbour’s, door to talk about their choice of religion.

Amend advancement of education

- The advancement of education should only apply where it is for the relief of poverty. A business is subject to tax and education is a business for some.

- This exemption might have been okay in an age when government did not provide free education to all. Now the exemption is sometimes to support people who want to make a choice about controlling their child’s education. That choice is their own and should not remove an obligation to contribute tax to the wider community.

Remove the donations rebate

- Donations should no longer generate a tax rebate. It is an administrative burden and has been subject to abuse. What you donate is your choice but once you can reduce your tax bill through a tax rebate/refund, it makes everyone a contributor to your personal choice. Let’s just keep it a personal choice.

- Previously there were arguments that services were not provided by government and this allows the gaps to be filled. In theory private enterprise can now fill those gaps and be self supporting. Government can assess the need and whether to fund that service or perhaps there are lower administration costs if government does it and that is an option.

- The current rules, the ‘Peter Dunne changes’, have allowed wealthy people to not pay any tax to government, but pay it all to their preferred charity. This creates a situation of winners and losers in funding rather than a spread of services to fulfil needs, and this is inefficient for the wider society. This is actually not charity or philanthropy but an undermining of community. If tax stays with the government we have better public accountability.

- And the experience with philanthropy is not great. The excess of charity to some, what a particular philanthropist thinks is the deserving charity means some charities become vehicles for the fantasies of the wealthy. A well reported example was Bill Gates’ misguided support for small schools in the US which arose from his misunderstanding of statistics. He thought small schools gave better academic achievements but the statistics did not say this. Huge waste and disruption followed his charity work.

The current rules on charities are undermining tax collection and our collective wealth. A rebate is undermining a citizen’s contribution to the wider society.

5. Remove GST as a tax (alternative taxes could be considered to replace if needed).

- GST is a regressive tax and is therefore completely unsuitable for a civilised society.

- The lie that the cost of GST equaled the lowering of income tax rates means nothing as time goes on and there is any negative disparity of salary and wage rises/changes and inflation. And this is what has happened, wages have not risen with inflation so it is not equal.

- GST undermines New Zealand businesses when competing with online overseas firms, for New Zealand purchasers. This especially impacts small New Zealand businesses. Overseas companies may or may not comply with our GST tax rules, and audit of overseas companies is a huge burden (it is questionable whether we even do it).

- GST runs counter to Keynesian economics as it suppresses demand from the poorest groups who spend all their money in the domestic economy and stimulate it. Taxation should be directed to the wealthiest people in society as the purpose of tax is redistribution. Recent history of stimulus payments (Japan to halt deflation, the US 2008 bank bailouts, and the US Trump budgets cuts) all gave stimulus to large businesses which tended to save the money or push it into their own stock prices, which did not stimulate the economy or make the lives of its citizens less harsh. These are repeated demonstrations of the ineffectiveness of pushing money into the supply side of the economy. Wants and needs are not being met but share prices have been sustained. We have witnessed the misapplication of Keynesian policies to deliver corporate welfare. The large business community is simply not that strong and effective at supplying wants and needs. We can all see this in our communities.

- GST has a lot of complexity in making time-consuming and finicky adjustments for private use of assets and on disposal of assets when the business is ceasing. It is easy to make mistakes and misunderstand what is required. By comparison an income tax on what has ‘come in’ without adjusting for capital/revenue or expenses is much easier. With this reset and no GST business people/owners particularly small owners would be primarily focused on running their business.

- The concept of taxation on consumer consumption may appeal to some people who want a less wasteful world, but GST does nothing to determine what is or isn’t consumed or the efficiency of its production.

- GST is misnamed. It is actually a tax on salary and wage income collected through the mechanism of people’s purchases. Unfairness arises as some wealthy people get their business or company to own all their assets. So a person can rent their house, their car, all their costs to run the house etc so that these can become costs for the business and GST is collected back through the business. Particularly if owned through a sequence of companies that link back to overseas companies possibly in a tax haven. And their own rent is in effect paid back to them as the beneficial owner. So all the GST from running the ‘business’ is ultimately recoverable to the beneficial individual.

- GST is a fundamentally unfair tax as it is primarily paid by salary and wage earners when it is supposed to be paid by all final consumers.

- GST is structured by zero rating to subsidise products for overseas consumers. This is damaging. See item D in ‘What are the main impacts from this reset?’ below.

- GST is conceptually flawed and failing for all the above reason.

6. Tax evasion (tax avoidance is in part dealt with by the above proposals) becomes fully supported by the New Zealand Police – financial intelligence unit.

- Tax evasion is one of the most serious threats to the health of our society and therefore to our democracy.

- The current growth of populist leaders is linked to the instability created by inequality which is in part driven by tax avoidance and evasion. Tax evasion must be taken very seriously and aggressively pursued, and any tax investigation work should be at least fully engaged with the New Zealand Police – financial intelligence unit. A threat of surveillance and criminality will be very sobering to the tax behaviour of the business community.

Summary of the six points

All these proposals are within the existing economic and tax structure and mostly only require simple changes to the existing rules. They are low cost to administer as there are fewer exceptions so fewer rules. Accounting rules would remain as they are. It is just tax rules that would change to focus on income only.

Transparency on the amount of tax paid

To support these changes private companies should be required to make public the income aspects of their accounts so a competitor who might be aware of what work is being done by that firm, could then assist or tipoff Inland Revenue if there is not compliance.

A non-individual’s contributions via tax to society should be celebrated and perhaps this should be available to the public. The purpose of entities within an economy is to create supply to meet demands for wants and needs and the supply of tax is part of that process so why should it be hidden, which was the previous assumption. Lack of transparency has not been helpful for combating tax evasion.

The seven principles guiding my reset changes above are:

- Tax will be seen as just a cost of business, like any other cost that can’t be evaded.

- These proposals do not completely erase tax avoidance but they go a very long way to doing that. Avoidance in future would primarily be about saying things aren’t income or the value of the income is not as much. There are other avoidance techniques like hiding ownership to pay a lower rate of tax. This is discussed a little more in Part C of this series.

- A level playing field for small and large businesses with a clearer focus on what they should be doing i.e. – providing goods and services (Including innovation and exports) not cost accrual competition.

- Better economic outcomes for consumers and local businesses.

- Simpler voluntary compliance.

- Low administration cost.

- Lower environmental costs.

What are the main impacts from this reset?

A. Businesses with a high cost structure would have to reflect these in the prices they charge to consumers and/or amend their expectations on a return from capital.

B. Businesses with a low cost structure would become very competitive in the provision of goods and services (competition would help temper the above price increases).

C. There would be an initial burst of inflation.

- We had to deal with the same situation on the introduction of GST. We currently have to deal with inflation for building materials and housing – it is a problem that exists regardless of the tax situation and it should not make us afraid of a necessary tax reset. But to deal with inflation –

- The removal of GST would assist at keeping inflation lower for consumers.

- Tax on gross income gives more income to the government to support beneficiaries/people in need, to counter negative impacts from inflation.

- Tax on gross income could allow a government to consider lower tax rates for individuals. But tax is already so low it is damaging society. A new consensus needs to emerge, that the collection of tax helps the economy and is an asset for business.

- A risk of runaway inflation needs to countered, i.e. some firms might ramp up prices to take short term economic revenge to try and return the status quo.

The government could partnership with a New Zealand company, or preferably go it alone, to have a supermarket facility to stock essentials or a range of goods. The government would fund the basic wholesale price using economy of scale purchases and then that preferred retailer or their own organisation would sell with only a 1% or 2% commission on those goods, and the government gets its money back on the wholesale sales (less some sale costs). Or

a percentage of expenses is able to be deducted. Like with property and interest deductibility. Only 75% allowed to deduct this year; then 50%; then 25%. This is not a good option as there is likely to be a rush to buy which might push up inflation.

- But inflation may not be as high as feared as some expenses are not hard cash costs, e.g depreciation, so there would not actually be a dollar for dollar rise in prices.

- Also large high cost structure businesses would have to drive down their spending plans and shift their business model to a low cost one. Business demand would drop off. This should keep inflation down. With the supply chain problem at the moment, that drop in business demand could push inflation down or steady it. It is the perfect time for a reset to occur.

- Also see point F below. If there are less steps between producer and consumer then there is less chance for inflation.

D. Our exports would cost more.

- This would create the correct incentive for New Zealand to add value to its products before export; creating jobs and innovation opportunities (e.g. in science, medicine, engineering) in New Zealand.

- For example, milk powder auctions. In the reset, production costs are now fully carried by the producer and not socialised to the taxpayer. To try and increase their revenue they are more likely to innovate to increase the return on their product, or go into vertical integration to access parts of the value add chain.

- Products sold by contract, for example, logs to China – our logs would cost more and they may – pay the high price, buy less, or not buy. If they don’t buy then we simply do not have a product that is worth selling. We would have to change that log/product using innovation, science and/or manufacturing, into something people did want to buy. Or move into something else.

- And there are Research and Development tax credits available to support innovation and they would continue to be available. (But I suspect a perverse situation will arise of getting R&D credits whatever the research. Perhaps the money for R&D is better spent by directly allocating more money to places like Crown Research institutes or tertiary institutions).

- In a sale negotiation a producer is aware of what a ‘profit’ will mean for them. Removing deductibility of expenses simply changes the base line for what that profit is. This happens now for any increase in cost.

- With the current tax system allowing costs to be socialised, it makes New Zealand taxpayers subsidise products for the benefit of overseas purchasers. It is creating an externality of some of the cost of production which sends the wrong signal about the use of resources and this is bad for the environment and economy.

- This creation of an externality is exacerbated by GST zero rating for exports (This is done so our goods remain more price competitive! The principle is the goods are not consumed in New Zealand so there is no GST but all the costs of production are deductible for GST). So all the services that went into supporting that export; education of people/employees, health services to look after people in the business, the courts that enforce laws that make doing business possible within New Zealand – al those costs of running a society are excluded from the cost price by the exclusion of GST to help fund them. Again the New Zealand taxpayer is being asked to subsidise the cost of goods and services supplied to overseas purchasers by having a reduced tax take. Yes the seller will return income from the sale and pay income tax (maybe) but those taxes are now too low. Using current tax system terminology; it is not income to the nation without taking account of the cost of production. This is just another reason GST is a terrible tax and should be dumped.

- Producers when negotiating a sale must have all the costs that contributed to that good or service in that cost price so the negotiation is real. Removing the impact of taxation and the services it supports is subsidising the sale.

- These reasons show that every country in the world would be doing the environment and their taxpayers/people a favour by moving to the reset changes here.

E. Speculative investments would become more risky.

- A traditional corporate raider might buy a company but as the cost to purchase is not deductible, each gross sale of the assets they strip off would be fully taxable. Tax on the sale of each asset could be more than the collective net profit.

- This is an important shift in the economy away from rewarding lazy asset stripping practises to businesses having to actually work and produce something to make their money.

- It would also take the pressure off prudent boards of directors who want to be cautious and careful and hold assets for a rainy day. These values/skills need to be protected as well as the push for innovation and value add, but not just asset stripping.

- If a company decided to buy another company but shortly after they changed their mind. That is a risk they had to calculate before they made the purchase as the sale will be taxable with no expense offset of the purchase price. This fact could pull down the number of potential purchasers which in turn could pull down the purchase price of businesses. And that may not be a bad thing because so many owners sell up for the capital gain and an easy life. Sales are often to overseas investors – who then turn the purchase price into effectively a loan to the business with the interest being tax deductible (subject to Thin Cap rules) and the loan repayments capital. So the choice to sell up would not be incentivised or rewarded with no tax as what happens now.

F. Middle men get squeezed

- The more sale and purchases between production and the final consumer the more the product will cost and the greater the amount of tax paid. This creates an incentive to have as few steps as possible between producer and consumer. Currently these middle steps layer in cost for the consumer as each step must make a profit for the function they fulfil. With the new rules the fewer the steps the greater your competitive advantage and the incentive to provide a cheaper product to the customer.

- Under this reset a local producer would correctly have the natural advantage of dealing directly with the local consumer. Somebody coming from elsewhere must have a special advantage (a quality or price) to undercut the local. A natural ‘green economic’ advantage will apply of supporting local production. Farmers markets would become even stronger by being price competitive.

- Existing business can adapt and achieve fewer steps by:

- Vertical integration – through different divisions of a large company instead of selling through separate companies or by using wholesalers. Perhaps supermarkets are close to this already?

- Producers being more online and visible online to skip any wholesale or retail outlet steps.

- Producers cooperating more and forming into physical or online markets, geographic online markets for easy delivery. The delivery person may be in partnership with producers? It will be clear business people will be avoiding intermediate sales (to reduce tax impact on the final consumer) by co-operating rather than sale transactions. Charging for service but not buying the product themselves.

- It is possible that dairies or private stores could become collection or distribution points for goods purchased?

- Being physically closer to their market.

- Supermarkets may have to reimagine themselves if producers band together to create virtual supermarkets. I can only speculate how these powerful supermarkets will react but they will be threatened by change as they have a high cost structure based on palaces in which to sell goods; unlike the less glamorous stores they once were.

G. Investment opportunities

- Investment opportunities (to start small businesses) would open up across the New Zealand economy especially in retail and hospitality because the big boys with high cost structures would not have the competitive advantages they currently get from ‘the normal principles of taxation’.

- Opportunities are likely to be with New Zealand based business who own their own premises or who can work from home, so are more community based. Many are potentially more artisan, e.g. artisan bread would be more price competitive with supermarket bakeries. Or small New Zealand clothing designers will become more competitive as they don’t have the high cost structure of central city retail stores (clothes produced overseas may still have cheaper costs but now the freight and retail costs will be fully reflected in the retail price allowing a New Zealand manufacturer to be more competitive).

- Further support of domestic production would be needed such as requiring certifications that goods imported are:

- recyclable, and there is a system in place to do it,

- made in a factory with people receiving a living wage in their nation,

- made in a way that is minimising damage to the environment or at least meeting any New Zealand standards.

- Certifications are likely to be open and anybody can challenge one. So info on where and when a good is produced is on the certification. An NGO or competitor could check the certificate and a fine made or withdrawal of goods made with a tax penalty? Options can be looked at. If critical goods are not able to meet these standards, then imports could continue but an active search for alternatives should be started in New Zealand.

- If we did not require imported goods to meet certain standards then we are undermining our domestic production, our environment, and the lives of citizens elsewhere. We are also perpetuating the exploitive process and systems (like the normal principles of taxation) overseas that damage people and the environment.

H. Increased visibility of criminal activity?

- The proceeds of crime need to be laundered and often this is about pushing transactions through several entities to hide it. But if sale and purchase agreements go through here in New Zealand entities, then they will be subject to tax. Almost all other legitimate businesses will be trying to minimise transactions.

- I’m sure they will find ways to be criminals but in theory it could be easier to find criminality or more easily get tax if found.

- As the Pandora papers show, more work needs to be done and this reset is the simplest and most effective way to help.

I. High turnover low margin activities would have to change their model

- Another challenge is businesses that rely on quick buying and selling for turnover. This applies to most retail chains in New Zealand and they will need to adapt to the new competition that would come as their prices will rise.

- The sharemarket may need some form of exemption but it seems like an institution that is not performing its function of raising capital that well. An investigation of how well it works for the economy is overdue. It tends to value speed over thought and financial bubbles tend to rise and pop as if it’s a boiling pool more than a secure investment tool to support investment across the economy.

- If an exemption was to be given then there would have to be trade limitations or money would pour in to try and make capital gains without the hard work of building infrastructure and having investment ideas. I think an exemption is not a positive or constructive step for the economy as it would enhance the distortion of investing for wealth rather than producing something for wealth. Money is just following money to puff up the sharemarket.

- If there was no exemption then the volumes of trades would significantly reduce. The risk is investment could not move into new enterprises without a fear of taxation. Options need to be explored. e.g a short period of time on a regular basis (yearly, monthly?) when trades could be done with perhaps a transparent register of planned trades for that date. The register could close off two weeks before the period. But large trades have to be registered a month or more before the close off. This gives greater security to the sharemarket and less chance of panics or too many people rushing on to one stock. These are just some basic ideas. Many people love the speed and urgency of the market but investors being able to see clearly and in time who is intending to buy and sell a certain stock will create a more reflective and balanced analysis and commentary on what is happening and steps can be taken to fix problems. The urgency back in the 2008 sharemarket crash shows the current system is too vulnerable to collapse.

- It should also be explored and options developed on how else the ‘purpose’ of the sharemarket can be delivered or organised. It seems a very fragile framework to conduct investment in. For example, there could be development funds set up for sectors of the economy – health, housing, education, roading etc. And people could invest into the fund or a project being run through the fund. Businesses could suggest projects or investments to be supported by each fund. The project or options would be assessed as to how well it would deliver the need that the fund is trying to support – investors could then chose where they wished to put their money. Businesses would compete for funding of their project. There is a lot of process to establish, but this would be a better way to marshal the investment strength of the state rather than the current sharemarket approach of ‘give us your money as we are big and doing well and we will find ways to invest your money’. This is just one option idea and needs more work. It just shows there are other ways of doing investment.

- With these development funds it is possible or likely that the sharemarket will just fade away into irrelevance, but if it works it will stay.

- The sharemarket is very much about the better known get the most investment as they are seen as more secure. Borrowing is often possible because of the share price, and debit financing is heavily driven by the tax advantages. This framework is a very blunt tool to stimulate production/supply of goods and services to meet wants and needs in the economy. The reset disrupts these assumptions because it removes the tax subsidy. A company still has the complete right borrow and nothing is stopping them from doing it, excepts the risks involved. This raises the prospects of evolving new ways finance can be raised. So alternatives are about funds or companies projects that people or funds could invest in are one possible way to go. There could be a small business fund for start ups. Investment markets or ‘exhibitions’ could be a bigger feature where investors meet producers to pitch ideas and have demonstrations of product etc.

- Ultimately capital regardless of anything I suggest or speculate here, will find a way to make money in the way they wish. Nothing is done here to stop that. It is just tax will not be available to subsidise it.

J. Large capital infrastructure projects

- Like they do now, they will struggle. There aren’t any oil refineries, aluminium smelters, or steel works lining up to move to New Zealand. Currently all large infrastructure work rely on significant government support to make them happen so we lose nothing by making expenses non deductible.

- The film industry is a political decision to support or not, like the America’s Cup. That situation just continues according to political choices like it always has. Remember by allowing expenses to be offset to income we reduce the tax collected so we the people in effect help pay for it. So it would be a more transparent process if it is clearly brought into the political sphere. There are far more benefits for stopping the allowance of expenses than leaving it as it is.

K. Accounting Reactions

- There would be moves by accountants/businesses to have ‘gains’ moved out of entities and to individuals, and called a capital gain to the individual and not subject to tax. Rules would be needed so assets and gains stay within the businesses or are taxed to the individual, rather than just being ‘loaned’ to the business. There are many great simple ideas but here is not the space to discuss them it is just an area of work to fix a small potential tax loophole that some will try and stretch open.

- Valuations of items sold will be an issue. Perhaps items will be under valued to reduce the tax payable. So independent valuation if there was a dispute, or if a sale was between related parties.

L. Different sectors have different impacts

- Using the table in ‘Part E – Impact on various sectors in New Zealand from making a Reset’

- The table shows approximate impacts. It is impossible to tell how much each business could preserve/increase profit by cutting back expenditure. But the table indicates areas where inflation is more likely to be high as costs are so high. And as said before this is an appropriate price signal.

- The following are just some examples of how impacts would play out across some sectors of the economy. Statistics New Zealand ‘Annual enterprise survey: 2017 financial year (provisional)’.

My purpose here is just to be indicative of impacts. It is not required information or essential to my central points of the economic impacts. I’m using it to reinforce two points:

- Firstly – the argument that non-deductible expenditure would have very different impacts in different industries, ergo it may not work equally. My central point is – that there is different impact is true, but that is not bad. Every sector and business in a sector must pay its way under the reset. Under current rules one sector or business can be in loss to subsidise another sector or business which ultimately favours large firms. For example: